(Today we’re leaving for London. Regular columns will resume on 11/1. In the meantime, if turbulence occurs, keep your tray tables in their upright and locked position and your hands inside the blog.)

John Dick, CEO of Civic Science, has a weekly newsletter that is worth your time. This week he asks:

“What if we’re just talking ourselves into all of this? Admittedly, I partied too much in college to get good enough grades to go to a respectable grad school to become an economist. I’m out of my league here.”

Dick wonders why economists are so sure that we can’t escape inflation unless we head into a deep recession. He also wonders (as does Wrongo) if currently, there’s a doomsday loop at work. It’s true that there are times when regardless of the news, the stock market goes down. More from Dick:

“Oh no! The job market is too good. Wages are growing too fast! Employees have too much leverage in the workplace! The dollar’s too strong! People’s homes are worth too much! We’re all screwed!!!”

The news media dutifully reinforces the doomsday loop. And who proffers answers? Very few. So, around we go, blaming the politicians in one Party for something they cannot solve, and neither can the other Party. And thus, the prophecy fulfills itself. On to cartoons.

Sunset, Cranberry bog, Yarmouth, MA – October 2022 photo by Jean Burns

Wrongo and Ms. Right are leaving on Sunday for a week in London. We’re arriving there just as the horse race for whoever will become the UK’s next prime minister will be clear to all. We’re expecting it to dominate the British news while we’re there.

On September 10, Wrongo said he wasn’t a fan of the now departed Liz Truss. He also said it was hard to believe her effort to revive the zombie concept that is trickle-down economics would go well with the UK already in a recession. She lasted just 44 days in office. Here’s a hot take from England:

Seems like a lot of turmoil for a small, low growth, densely populated country.

Truss’s sin was simple. Her economic plan was designed to satisfy libertarian think tanks and fans of Ronald Reagan and Margret Thatcher rather than to be something workable. Republicans in America do this kind of thing because we can, since the dollar is the world’s reserve currency. That means we can go almost as far into debt as we want without the markets panicking.

But the UK doesn’t have that luxury. So there’s a limit to how many favors they can do to their own fabulously rich citizens.

The policy that got Truss thrown out of No. 10 Downing Street was a copy of the foundational Republican US domestic agenda, as practiced from Reagan to Trump. That is, cut taxes for the rich and corporations, then hope it eventually creates tax revenue before it forces spending cuts.

And the British financial markets seem to actually care about the well-being of their country’s economy. However, American markets seem to care only about maximizing share prices and the after-tax compensation of top-level executives.

US Conservatives were delighted when Truss became PM. On September 23, Larry Kudlow said on FOX:

“The new British prime minister, Liz Truss, has laid out a terrific supply-side economic growth plan which looks a lot like the basic thrust of Kevin McCarthy’s Commitment to America plan.”

Needless to say, like Truss, Republicans are also willing to do unfunded tax cuts and call it a growth agenda. They’re also willing to fail to extend America’s borrowing limit, in order to make their agenda happen. The GOP would try to hold the Democratic president hostage in order to share some political responsibility for that action, never mind that an American debt default would also hold a gun to the global economy.

That isn’t possible in the country that brought you Maggie Thatcher. They toss out their incompetent supply-siders. The elephant in the room of the UK’s chaos and crisis is 2016’s Brexit. Even though Brexit has brought about low GDP growth, it remains a hard right political project rooted in a mythical British past.

Brexit’s Tory supporters didn’t care about the hard economic evidence that Brexit would be an act of economic self-harm. And the political divisions Brexit caused in the Tory party remain a problem as they now seek to unite behind another sacrificial PM. From David Frum:

“The problem is that you’re not eligible for the captaincy unless you agree it was a brilliant idea to scupper the ship in 2016 – and can convincingly act baffled why it has been sinking ever since,”

If America still has the ability to learn, it would be great if they studied this Tory disaster.

It would be nice if American voters would really punish Republicans when they fuck up and tank the economy again. And not just by electing a Democratic president, as they did in 1992 and 2008 when the economy went south.

OTOH, if anything can get Joe Biden reelected, it’s a Republican-led Congress in 2023 and 2024. They will screw things up just as thoroughly as Liz Truss has screwed the pooch in Britain. Then, we’ll have to see if they’ll ever be blamed for it.

Enough foreign politics for today. It’s time for our Saturday Soother, where we consider raking the leaves that are suddenly carpeting the Fields of Wrong but decide to put it off until we return.

Let’s start by brewing up a big mug of Costa Rica Cerro Dragon Geisha Honey ($12.00/4oz.) from RamsHead Coffee Roasters of Bozeman, Montana. It is said to be an invitingly complex Costa Rica honey-processed cup with notes of tropical fruit, sweet herbs, and crisp cocoa.

Now grab a seat by a south-facing window and listen to Khatia Buniatishvili play Schubert’s “Impromptu No. 3 in G-Flat Major, Op. 90, D. 899”. It isn’t played in front of a live audience, so no coughing, etc.

Schubert wrote eight solo piano pieces called impromptus. An impromptu is a musical work, usually for a solo instrument, in this case, piano. Schubert composed this work the year before he died:

Snake River, Grand Teton NP, WY – October 2022 photo by Hilary Bralove

Yesterday, Wrongo said that the Dems should add a focus on inflation and the economy to their closing argument when asking voters to keep them in power. Here’s a suggestion of what that argument might look like from David Doney (@David_Charts on Twitter). Doney draws his stats from the Federal Reserve Economic Data (known as FRED) and the Congressional Budget Office (CBO). Below is an extract from his Twitter feed:

Jobs: More Americans are working than at any time in history: 153 million. The economy now has 500k more jobs than it did before the pandemic. The unemployment rate is 3.5%, the lowest since 1969. With more people working there’s more spending.

Wealth: The bottom half of US households have an average real net worth of $67,200, the highest ever. Under Trump, it was just $34,648. (While Trump gave tax cuts to the wealthy. Biden gave them to the middle and lower class.) Even those in the 50th to 90th percentile are doing better under Biden: average real net worth is now $747,010 vs. $699,530 under Trump. It’s important to remember that these are averages not median net worth numbers, which are lower. Median net worth in the US is $121,700, up 17.6 % from 2016.

Income: Real wages are higher than before the pandemic. Despite what some pundits say, they have outpaced inflation. From February 2020 to last month, wages for production and non-supervisory workers have risen 15.6%, while the Consumer Price Index (CPI) has risen 14.6%. So Americans’ purchasing power is greater today than it was in 2019.

The deficit: Our annual federal budget deficit is 50% lower than it was last year. It was $2.8 trillion in fiscal year 2021 and is $1.4 trillion this year, according to CBO estimates. Government income is up and government spending is down: Revenues are $850 billion (or 21%) higher and spending is $548 billion (or 8%) lower.

This continues the historical pattern of Democratic administrations being more fiscally responsible than Republicans. Yet the GOP’s closing argument includes screaming about Democratic spending which they say caused inflation. They are trying to convince Americans who either don’t read or bother to check facts that it’s the Democrats who spend like crazy. The opposite is true.

The economy: The Gross Domestic Product (GDP) hit an all-time high of $20 trillion in the fourth quarter of 2021, and currently is $19.9 trillion (for the second quarter of this year). The Atlanta Fed thinks GDP will grow 2.8% in the third quarter. So no recession just yet. In fact, Doney reports that the six key indicators that the National Bureau of Economic Research (NBER) uses to decide if we’re in a recession were all up from June to September.

Health insurance: Biden revived the Obamacare signup campaigns and advertising that Trump had eliminated. And now 92% of Americans (and more than 98% of kids) have health insurance, an all-time high. Before Obamacare, close to 18% of Americans had no health insurance.

There’s no doubt that many Americans are worried about the high prices at the grocery store and at the gas pump. But one reason inflation has increased is because people have more money in their pockets. Americans have $4 trillion more in their bank accounts than they did before the pandemic. So they’re working, earning money, and spending it.

The other factor driving inflation is the consolidation of companies into just a handful of major corporations, and the ability of those corporations to jack up prices. Corporate profits are at a 70-year high, yet American corporations are still raising prices. They’re doing so because there’s so little competition.

Republicans in Congress won’t stop corporate price gouging. And we know the GOP will blame Dems for high federal spending (which, as said above, is down 8% so far vs. last year). But the GOP won’t let the facts get in the way of their bad policies. They’ll use this manufactured crisis, along with refusing to raise the debt ceiling, to try to force Democrats to support cuts to Social Security, Medicare, and other social safety net programs.

“It is such a good question to ask what the Republicans will do if they gain control. We obviously know the answer. They will block anything and everything that might help people so they can blame Biden for [it in] 2024.”

The Democrats’ closing argument needs to include a strong, populist message. They should be saying that Democrats believe people must come before profits. Dan Pfeiffer reports:

“The folks at Data for Progress tested a series of messages on inflation and found that emphasizing corporate greed was an effective pushback on concerns about inflation.”

OTOH, the inflation and economic message must be carefully crafted. It could backfire with some who have missed the current jobs market and are struggling to pay their bills.

Democrats should acknowledge the pain caused by high prices while pointing out that a strong economy and the Party’s fiscal responsibility are helping many people cope with higher prices today and will help to reduce inflation in the near future.

Blueberry barrens, Sedgewick, ME – Via. The blueberry plants turn red like trees because they’re also preparing for winter dormancy.

We’ve been writing about how the threat of losing both the House and Senate weighs on Democrats. Inflation and the economy are said to be voters’ top concerns in recent polls. This week’s NYT/Siena College survey showed that 26% of respondents cited the economy, while another 18% chose inflation as their No. 1 issue.

The Dem’s lack of messaging about inflation needs to be adjusted because inflation is hitting hardest in a few swing states like Georgia, Arizona, and Florida. From the Right-leaning Washington Times:

“The Phoenix metropolitan area has the highest inflation rate in the nation at 13%, the worst of any US city in more than 20 years and twice as high as the rate in San Francisco. It’s a high hurdle for Democratic Sen. Mark Kelly of Arizona as he tries to fend off a challenge from Republican Blake Masters.”

Wallet Hub says that the US metropolitan area with the second-highest inflation rate is Atlanta, where consumer prices are 11.7% higher than a year ago. Senate Democratic incumbent Raphael Warnock holds a four point lead. One message that’s lost in the inflation debate is, as Georgia’s Sen. Warnock says:

“While we are seeing record prices, a lot of our corporate actors are seeing record profits in the gas industry and the pharmaceutical industry.”

Two metros in Florida: Miami, Ft. Lauderdale, and West Palm beach (10.7%), along with Tampa-St. Petersburg (10.5%), are in the top four highest inflation cities, and Marco Rubio (R) holds a 4.7-point lead, with Democrat Val Demings having an uphill fight.

Philadelphia ranks 14th in metropolitan area inflation, at 8.1%. Democratic Senate candidate John Fetterman leads by 2%.

Nationally, the inflation rate is 8.2%.

Nearly two-thirds of consumer spending goes to services rather than products. Services are now the key driver of US inflation. The CPI for services increased in September for the 13th month in a row, and by the most since 1982. Housing costs spiked, but so did other services, such as health insurance (up 28% year-over-year). Airline fares rose by 42.9%, while motor vehicle maintenance and repair rose by 11.1%.

One of the worst categories is the CPI for “food at home”, or food bought in stores and at markets. It spiked by 0.7% in September from August. Year-over-year, the CPI for food at home jumped by 13.0%, led by eggs which are up by 30.5%. Food inflation is particularly insidious because it hits lower-income consumers the most, since they spend a larger share of their budget on food.

The key question for Democratic candidates in swing states during the last weeks before the midterms is how to talk about the economy when inflation remains above 8% and maybe is even higher in their state.

Democratic strategist Mike Lux has warned that Democrats can’t duck talking about inflation at a time when it’s the Republicans’ primary campaign issue. Lux says how Democrats should explicitly address inflation:

Wealthy corporations with monopoly power are jacking up their prices, and their profits are going through the roof.

Drug prices and health insurance premiums are going to go down because of the Inflation Reduction Act…while Republicans have no plan of their own.

But Dems should also ask why voters think that if Republicans return to power that they will actually fight against inflation and improve the economy? If they get back in power all they’ll offer is tax cuts and financial austerity. They’re saying they will jeopardize the future of Social Security and Medicare.

Their House Speaker-in-waiting, Kevin McCarthy (R-CA) has said in an interview with Punchbowl that he will hold the national debt ceiling hostage next year, a move that the WaPo’s Catherine Rampell warns “could easily precipitate a global financial catastrophe.”

The economy is a difficult issue for Dems this year, and many are afraid to talk about inflation. But they have an excellent legislative record to run on and the best job market in 40 years. Democrats have plenty to say about inflation if they connect it to broader economic themes where they have a strong message.

For sure, Dems can talk about Republicans’ appalling destruction of reproductive rights, but we can’t expect to win the election on that alone.

Liz Truss’s big bet since taking over as UK prime minister is to lower taxes just like St. Ronnie and Trump did in the US. Said Truss:

“Lower taxes lead to economic growth, there is no doubt in my mind about that,”

Trickle down will work this time, we promise, say UK Conservatives.

The tax reductions will require the UK government to borrow bigly to balance their budget. They hope that there will be so much growth that the UK will make it all back in future tax payments. Just like in the US, the lie is that these tax cuts will pay for themselves! Something that has never happened.

The UK Treasury said that the top personal rate will be cut from 45% to 40%. That will be more beneficial for the wealthy than the majority of British society. Shortly after the cuts were announced on Friday, the pound sank almost 2.6% to its lowest level against the US dollar since 1985. Wrongo hates to quote Larry Summers, but he said this:

“The UK is behaving a bit like an emerging market turning itself into a submerging market…it is pursuing the worst macroeconomic policies of any major country in a long time.”

“Liz Truss just announced the UK’s biggest giveaway to the rich since 1972, which resulted in an IMF bailout. Now the pound is crashing in the middle of the worst inflation since the 70s. Bold strategy….Let’s see if it pays off.”

It’s hard to believe this will go well with the UK already in a recession. On to cartoons.

Morning light – Norbeck Pass, Badlands NP, SD – July 2022 photo by Rick Berk Photography

After imposing sanctions on Russia for their invasion of Ukraine, Germany and all of Europe are now facing an energy crisis unlike ever in their history. Gas deliveries from Russia have been halted altogether, exposing the dependence of European energy consumers on pipelined gas from Russia.

Strategically, Germany’s dependence on Russia is a muddle. Germany has depended on Russian natural gas since the Cold War. And it steadily increased its reliance on Russian gas while reducing alternative sources of energy such as nuclear power, even after Russia invaded Ukraine in 2014.

On September 5th, Russia said it would close its Nord Stream I pipeline for as long as Western sanctions are in place. This initially sent gas prices higher by 30%. They currently stand at around $400 expressed as the equivalent of a barrel of oil.

The energy shock has morphed into a political and economic shock. In Germany, steelmaker ArcelorMittal is shutting down a plant in Bremen. Germany is spending €65 billion (1.8% of GDP) on measures including a price cap on electricity for households and firms.

France has enacted a retail price freeze for energy. French gas prices are frozen until at least the end of 2022, and the rise in electricity prices is capped at 4%.

Now, 14% of families in England are behind on their utility bills. The UK’s prime minister Liz Truss unveiled a plan to freeze prices for two years, which could cost more than £100 billion (4.3% of its GDP) and will be financed through government borrowing.

But the threatened loss of Russian gas also caused European governments to make big changes by lowering demand and lining up new gas supplies. That has lowered gas futures prices. From Wolf Richter:

“The front-month October TTF contract in the Netherlands – a benchmark for northwest Europe – plunged by 8% on Monday from Friday, and by 44% from the peak on August 26, to €191.02 per megawatt-hour (MWh) at the close today…”

On the supply side, the Netherlands has started operations of two floating liquefied natural gas (LNG) import and storage terminals in the port of Eemshaven. These floating storage and regasification units (FSRU) receive the LNG, store it, re-gasify it, and then send the natural gas via pipeline into the land-based distribution network in the Netherlands, from where it can be further distributed throughout Europe. Three more FSRUs are planned.

Germany had failed to build a single LNG import terminal as an alternative to Russian piped gas, but it has now chartered five FSRUs, three of which will start operating this winter. Germany has also been filling its gas storage facilities at record pace. They are currently 87.9% full, according to Gas Infrastructure Europe. For the EU overall, storage facilities are 83.6% full, well above the EU’s 80% target.

Strategically, Germany (and the EU) can’t simply return to the old normal once (IF) Ukraine hostilities end. Germany’s vulnerability to its natural gas dependence on Russia has irrevocably shaken up the economies and politics of Germany and most of Europe.

Germany seems to have finally figured this out. In the short run, (2-3 years) the consequence will be that Germany’s and EU’s consumers and industrial users will face natural gas prices that are much higher than they were two years ago. Higher-cost LNG will be a larger part of the energy mix, with low-cost pipeline natural gas from Russia a smaller part.

As Wrongo said recently, Russia cannot easily sell all of the natural gas that it’s not selling to Europe, because the pipelines can’t be moved overnight. And Russia has no LNG export facilities linked to its production sites. So Russia will have to cut some production at these sites and will lose the revenues associated with that lost production.

Also in the short run, Europe’s governments will struggle to balance relief for its citizens against letting energy prices rise high enough to discourage use. These governments are scrambling to find alternative sources while cutting consumption as deeply as they can. But winter is coming, and if they aren’t able to find successful workarounds, economic growth will slow, and European voters may demand that their governments drop sanctions on Russia.

That is a political problem that Russia hopes to exploit this winter.

Europe’s response to the Russian invasion of Ukraine has exposed both its vulnerability to Russian gas, and also the poor strategic decisions that it and Germany have made over several decades: to take the cheapest, simplest solution to Europe’s growing energy needs.

Russia is hoping that it will gain some leverage in the diplomacy regarding an endgame in Ukraine and the anti-Russia sanctions regime this winter.

And like always, regardless of the outcome, no politician will be harmed while playing this game.

“The 140 years from 1870 to 2010 of the long twentieth century were, I strongly believe, the most consequential years of all humanity’s centuries.”

Matthews thinks it’s a bold claim. After all, homo sapiens has been around for at least 300,000 years; DeLong’s “long twentieth century” represents 0.05% of that history.

But DeLong says an incredible thing happened during that sliver of time that had eluded our species for the other 99.95% of our history: Before 1870, technological progress was glacial, but after 1870 it accelerated dramatically. More from Vox:

“DeLong reports that in 1870, an average unskilled male worker living in London could afford 5,000 calories for himself and his family on his daily wages. That was more than the 3,000 calories he could’ve afforded in 1600, a 66% increase….But by 2010, the same worker could afford 2.4 million calories a day, a nearly five hundred fold increase.”

DeLong is speaking of the nations of the rich north, not about all nations. He’s saying that food surplus was the key driver of progress. What’s implied is that the greatest difference between the wealthy and everyone else was that the poor were living on the verge of starvation. Those basic economic facts shifted once having enough to eat ceased being society’s most critical status distinction.

Another interesting statistic from the book:

“…the average number of years of a woman’s life spent either pregnant or breastfeeding…has gone down dramatically, from 20 years of a typical woman’s life in 1870 to four years today.”

Most historians present modern history as a long 19th century (from the French revolution in 1789) to the crisis of 1914. Which is then followed by a shorter 20th century ending with the fall of communism. DeLong, by contrast, argues that the period from 1870 to 2010 is best seen as a coherent whole: the first era, he argues, in which historical developments were overwhelmingly driven by economics.

“…despite the Industrial Revolution…for millennia, technological improvements never yielded enough new production to outrun population growth. Incomes had stuck close to subsistence levels. Yet from around 1870, growth found a new gear, and incomes in leading economies rose to unprecedented levels, then kept climbing.”

DeLong says that economic policy in this period was a duel between the ideas of Friedrich von Hayek, who extolled the power of the free market, and Karl Polanyi, who warned that the market should serve man, not man serving the market.

Before WWI, markets generated rapid growth along with soaring inequality. People pushed back, demanding greater political rights, which they used to pursue regulation of the economy and improved social insurance.

After WWII, a mix of a market economy and a generous safety-net made for a happy marriage of Hayek and Polanyi, improved by Keynes, who said that governments should act to prevent economic recessions. This led to a three-decade post-war period of growth unmatched before or since. DeLong calls them the Thirty Glorious Years; from 1945 to 1975, as the US and Europe recovered from World War II.

But when growth sagged and inflation rose in the 1970s, voters supported politicians promising market-friendly, or “neoliberal”, economic growth reforms, like lower taxes and reduced regulation. But those reforms didn’t keep economic growth high. And they also led to even worse inequality. Still, the US and other rich countries pressed on with them, right up to the 2008 global financial crisis, which marks the end of DeLong’s 20th century.

According to a paper by Carter C. Price and Kathryn Edwards of the RAND Corporation, had the more equitable income distribution that America experienced in those thirty glorious years stayed constant, the aggregate annual income of Americans earning below the 90th percentile would have been $2.5 trillion higher in just the year 2018. That’s an amount equal to nearly 12% of GDP.

Price and Edwards say that the cumulative inequality cost for our 40-year experiment in government-supported income inequality added up to $47 trillion from 1975 through 2018. And probably equaled $50 trillion by 2020.

That’s $50 trillion that would have made the vast majority of Americans far more healthy, resilient, and financially secure.

So, the big unanswered question is: Can we again return to a period where we see both economic growth and equitable growth? It’s highly doubtful. As DeLong says in Time:

“Our current situation: in the rich countries there is enough by any reasonable standard, and yet we are all unhappy, all earnestly seeking to discover who the enemies are who have somehow stolen our rich birthright and fed us unappetizing lentil stew instead.”

The problem here is that our entire culture, economy and even our civilization is predicated around growth and people haven’t known anything else. Hope you’ve enjoyed the ride.

Time to wake up America! We need to reimagine capitalism, our taxation policies and our welfare scheme if we are to survive. Expect a rough adjustment. To help you wake up, listen, and watch Bruce Springsteen perform “Darlington County” live in London in 2013:

Good strategy is supposed to include a look at what the logical outcomes may be, once you’ve implemented your strategic plan. Was that done when the US and the EU decided to sanction Russia about its Ukraine invasion after having sanctioned Iran, well, for being Iran?

When you treat much of the world as your enemy, you should expect them to eventually find common cause and fight back. We’re speaking about the world’s supply of natural gas (NatGas). There is a new alliance between Russia and Iran on NatGas. At Oil Price, Simon Watkins says that a new energy cartel is forming: (brackets and emphasis by Wrongo)

“The US $40 billion memorandum of understanding (MoU) signed last month between [Russia’s] Gazprom and the National Iranian Oil Company (NIOC) is a steppingstone to enabling Russia and Iran to implement their long-held plan to be the core participants in a global cartel for gas suppliers in the same mold as the Organization of the Petroleum Exporting Countries (OPEC) for oil suppliers.”

The article describes how Russia and Iran are creating a NatGas OPEC. The two countries are first and second respectively in holding the world’s largest NatGas reserves. Russia has just under 48 trillion cubic meters (tcm) and Iran has nearly 34 tcm, so the two countries are in an ideal position to form a cartel.

NatGas is a vital commodity. It is widely seen as the optimal product in the transition from fossil fuels to renewable energy. And controlling the global flow of it will be the key to energy-based power over the next 10 to 20 years. This has already been demonstrated in Russia’s hold over the EU through its NatGas supplies.

From a top-down perspective, this Russia-Iran alliance might also draw other Middle East gas producers, who have tried to be neutral between the Russia-Iran-China axis or the US-EU-Japan axis.

Qatar has long been seen by Russia and Iran as a prime candidate for this kind of gas cartel because it shares its gas field with Iran. Iran has exclusive rights over 3,700 sq.km of the well-known South Pars field (containing around 14 tcm of gas), with Qatar’s North Field comprising the remaining 6,000 sq.km (and 37 tcm of gas).

If they can enlist Qatar, this new cartel would control 60% of world gas reserves, allowing them to control NatGas prices globally. It would be logical for prices to rise, given the growing demand for NatGas in the coming decades.

But this means that in a decade or so, the US, Europe, and Asia will all be more dependent on imports from Russia, Iran, and Qatar, while competing with the rest of the world for our share in order to maintain our economy and lifestyle.

So, strategy can be a bitch. By creating a global political and economic environment that pushes Russia, Iran, and Qatar into a cartel, we’ve created a significant future economic vulnerability.

“…about 1 in 6 American homes…have fallen behind on their utility bills. It is, according to the National Energy Assistance Directors Association (NEADA), the worst crisis the group has ever documented. Underpinning those numbers is a…surge in electricity prices, propelled by the soaring cost of natural gas.”

That’s 16% of American homes for the math challenged. Winter in the US may not be as big a disaster as in the UK and Europe, (better insulation). But plenty of people here will have to choose between food and heat.

The world is sorting itself out into blocks of countries aligned with each other. Russia, China, Iran and perhaps India, want their own commodity-based financial system to reduce their exposure to the political impacts from the West’s corporate/state “free” market system, which has used trade as a weapon for the past few decades.

There are two ways of looking at this. We could just build this energy vulnerability into our economic planning and prepare to devote a growing share of our GDP to paying the cartel for more NatGas.

Or, we could immediately start seriously building out our renewable energy capacity. There’s a model. Europe is attempting to pivot away as quickly as possible from its dependence on Russia.

We could do the same thing.

That could reduce our exposure to imported NatGas because it’s largely a bridge from coal to renewables. Massive investing in renewables would give Russia and Iran a shorter bridge than they think they’re getting.

Stormy view from House Mountain, Sedona, AZ – August 2022 photo by Ed Mitchell

Tens of thousands of teacher openings are unfilled as students head back to American classrooms. That’s prompting states and school districts to try everything they can to address the teacher shortage.

Except increase their pay. The Economic Policy Institute (EPI) has tracked teacher compensation for 18 years. Here’s the headline:

“…teachers are paid less (in weekly wages and total compensation) than their nonteacher college-educated counterparts, and the situation has worsened considerably over time.”

EPI tracks what they call the relative teacher wage penalty, the relative wages and total compensation of teachers compared to other college graduates. Here are the EPI’s findings:

Inflation-adjusted average weekly wages of teachers have been relatively flat since 1996. The average weekly wages of public school teachers (adjusted for inflation) increased just $29 from 1996 to 2021, while inflation-adjusted weekly wages of other college graduates rose from $1,564 to $2,009 —a $445 increase.

The relative teacher wage penalty reached a record high in 2021. It was 23.5% in 2021, up from 6.1% in 1996. The penalty was worse for men than for women. The penalty for men rose from 18.6% to 35.2%.

The great portfolio of teachers’ benefits used to be a selling point, but it hasn’t been enough to offset the growing wage penalty. The teacher total compensation penalty was 14.2% in 2021 (a 23.5% wage penalty offset by a 9.3% benefits advantage).

The relative teacher wage penalty exceeds 20% in 28 states. Teacher weekly wage penalties estimated for each state range from 3.4% in Rhode Island to 35.9% in Colorado. In 28 states, teachers are paid less than 80 cents on the dollar earned by similar college-educated workers.

The EPI has a chart showing the relative erosion of teacher wages vs. other college graduates since 1980:

The EPI focuses on “weekly wages” to avoid the comparisons of length of the work year (i.e., the “summers off” issue for teachers).

Add to this the general decline in working conditions for teachers, and many who are eligible for retirement are leaving. Republicans in particular are politicizing education. Some are pushing the idea of “parental rights.” That is happening in Florida, Texas and in other states. It’s clear that in some school districts parents want the right to censor what’s being taught. Some Conservatives are pushing for a camera in every classroom across America. Tucker Carlson called for cameras in classrooms to “oversee the people teaching your children, forming their minds.”

This comes under the guise of “transparency in the classroom”, parents keeping an eye on teachers, so they won’t teach the dreaded Critical Race Theory (or groom kids to become trans, or gay). Teachers naturally bristle at the idea of video auditing.

Forcing teacher compliance with imposed politicized curricula won’t make these jobs any more desirable.

Some states are relaxing licensing requirements to make it easier for people to fill some of those unfilled jobs. Florida, which has about 8,000 open teaching positions, is allowing military veterans without a bachelor’s degree and no prior teaching experience to apply for a temporary five-year teaching certificate while they finish their bachelor’s degrees.

The biggest issues to solve are better public school funding, which can help end the teacher wage penalty. That requires towns to raise taxes. Second, the politicization of education is changing the amount of parental control in the day-to-day operations in some school districts. That’s making teaching an even lower-status job than it is now.

According to the BLS, there are currently 300,000 fewer teachers nationwide compared to before the pandemic. Part of this is job satisfaction. A survey from the American Federation of Teachers found that 74% of teachers were dissatisfied with their job, up from 41% two years ago.

If teachers and staff are underpaid, under-resourced and are now being second-guessed in the classroom, they’re not going to stay. So replacing them will become an even bigger problem.

Enough of this week’s problems, it’s time for our Saturday Soother! Let’s put Trump’s secrets and Liz Cheney’s political prospects on pause. We’re facing moderate drought conditions here in CT, so lawn mowing has ceased, and our grass is brown and crunchy.

But, it’s time to empty our minds, so that we can begin filling them up again on Monday. Start by grabbing a cold glass of lemonade and a seat in the shade.

Now, watch and listen to Antonin Dvorak’s “4 miniatures”, for 2 Violins and Viola, played here by the Musicians of Lenox Hill at Temple Israel of the City of New York in April 2019:

As discussed yesterday, polls are showing that voters are still concerned about inflation. The good news over the past two days is that producer prices (prices at the wholesale level) and consumer prices both fell from June to July.

But these inflation concerns won’t be going away, and the Republicans hope to make the November midterms a “gas and groceries” election, saying Biden is the cause of rising prices. In July’s Consumer Price Index, the price of groceries was a particular pain point, rising 1.3% for the month. Wolfstreet reports that the year-over-year rise in the “food at home” part of the CPI (food bought in stores and at markets) is now at 13.1%, the worst spike since 1979.

Food is a category where inflation hits consumers right in the face on a daily basis. And it hits people on the lower end of the income spectrum much harder because they spend a relatively larger portion of their income on food.

But the fall in gasoline prices over the last couple of months is also meaningful. After peaking in June at $5.03 per gallon, the average national price of gas fell below $4 this week, according to GasBuddy.

The Hill reports that Biden will go on offense against the Republicans’ drumbeat about inflation by traveling the country to tout job creation and the Inflation Reduction Act, once it is passed by the House on Friday. Biden plans to make the point that Congressional Republicans sided with the special interests every step of the way on delivering lower costs for working people.

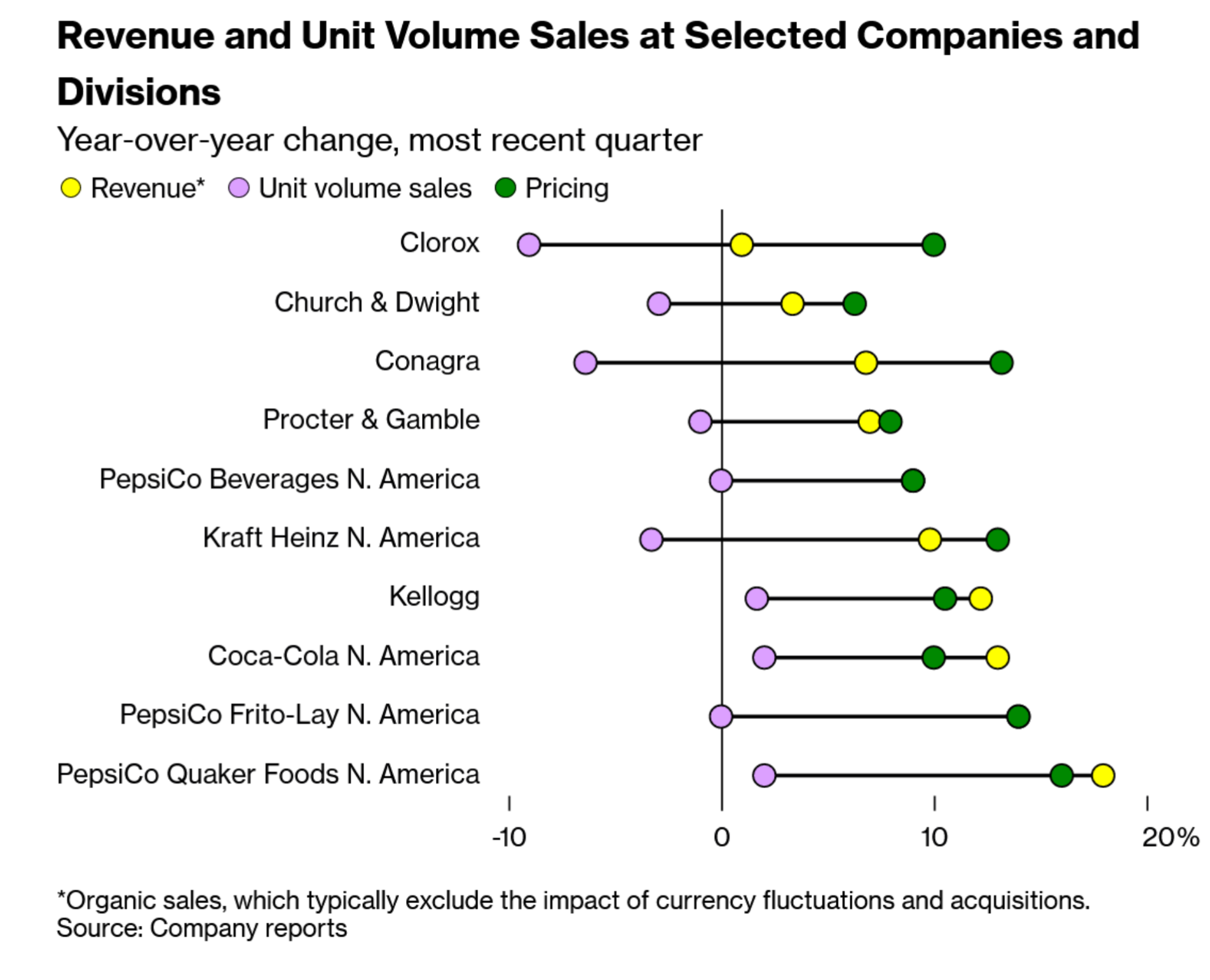

“The first sign that this wasn’t going to be a typical corporate earnings season came early on the morning of July 12, when PepsiCo Inc. unveiled an odd set of results. Growth in unit sales, it said, was essentially zero in North America. Revenue rose though, driven by the double-digit price increases Pepsi slapped on its snacks.”

They weren’t the only consumer product company to raise prices as sales fell: The purple dots show how unit sales fell (as much as 10% for Clorox) while prices (green dots) rose in most cases, more than 10%. And revenue (yellow dots) rose for all firms:

This is bad for the economy on many levels: Price-driven sales growth isn’t healthy; and it isn’t good for consumers who have lost purchasing power (and are angry about it). It isn’t good for our overall economy, or for the Federal Reserve that’s trying to bring down inflation.

Many CEOs are willing to raise prices because it’s no longer the taboo it has been for the past two decades, when annual inflation averaged a little more than 2%. Their thinking is that if volumes slip a little as a result of the price hikes, their share prices won’t take a beating. So no worries, just raise prices.

The bet that these consumer products CEOs are making is that once things settle down in the economy, people will come back. Bloomberg quotes Neil Saunders, an analyst at GlobalData Plc, a consulting company:

“If they keep losing share next year, they’ll take more notice. It’s very hard at the moment to tell what’s temporary and what’s permanent.”

Starbucks, Coca-Cola, Kimberly-Clark, and Church & Dwight, the maker of Arm & Hammer baking soda and OxiClean, all reported quarterly numbers that fall into the weak-volumes-and-big-price-hikes category. More from Bloomberg: (emphasis by Wrongo)

“One of the best examples is Conagra Brands Inc., the…Chicago-based food conglomerate, which reported results on July 14. A core measure of its revenue jumped 6.8%, in the three months that ended on May 29, thanks to an increase of 13% in the average price it charged….The amount of goods it sold, though, fell 6.4%.”

We know that inflation is very high, among the highest rates in the past 40 years. It now seems clear that consumer products companies are a prime contributor to these price increases.

We know that unemployment is as low as it’s been in 50 years. The labor market is strong. We know that the growth rate of GDP was really high in 2021, and that it’s slowing in 2022.

What we don’t know is how voters are going to act in November.