The Daily Escape:

Super bloom, Carrizo Plain NM, CA – April 2023 photo via Today’s California

Bed Bath and Beyond (BBBY) filed for Chapter 11 bankruptcy on April 23. It said it will liquidate its assets and close its remaining stores unless it can find a bidder for the 360 Bed Bath and Beyond stores and for the 120 buybuy BABY stores.

A little history: A year ago, the prices of their bonds began to collapse. By August 2022, suppliers halted shipments due to unpaid bills. When this became public, its 30-year bonds, issued in 2014, plunged to 16 cents on the dollar (last Friday, they were at about 5 cents on the dollar).

From Wolf Richter:

“While all this was going on, the company promoted its latest turnaround plan and closed hundreds of stores. But you can’t turn around a failing brick-and-mortar retailer. On January 5th this year, the company issued a “going concern” warning.”

There are at least three lessons to take away from the BBBY story: First, they are the latest victim of the move to online shopping. People trusted Bed Bath & Beyond, and they had a pretty good e-commerce business. They could have done very well with it if they had accepted 10 years ago that they needed to phase out of their brick-and-mortar stores.

But brick-and-mortar retailers have difficulty letting go of their brick-and-mortar storefronts. They just can’t explain to their investors that their huge, fixed investment in physical stores are doomed and need to be closed.

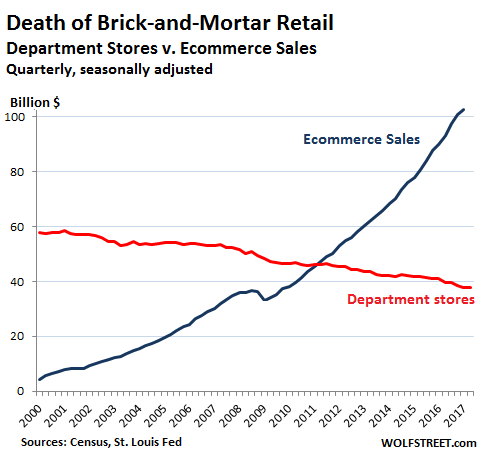

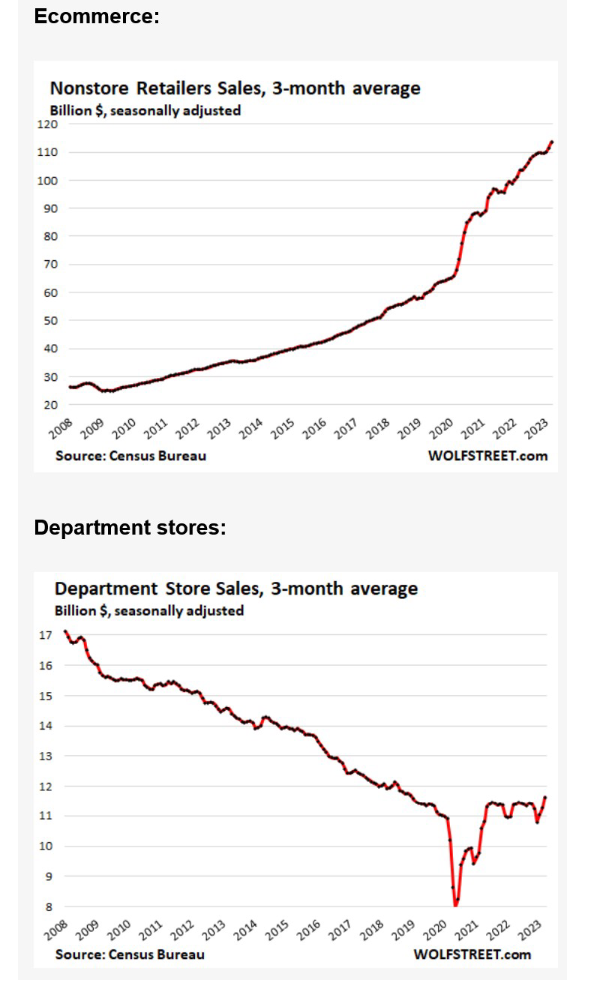

Wolf has two great charts comparing the rapid growth in e-commerce and the steep drop in sales by brick-and-mortar retail over the past 15 years:

These two charts show that e-commerce basically replaced $5-9 Billion in annual in-store sales for the retail industry. The top chart shows that e-commerce had reached about $115 billion by 2023. The lower chart shows that in-store sales fell from $17 billion per year in 2008 to a low of $8 billion in 2020 before recovering to nearly $12 billion in 2023.

The second issue was that rather than investing in their business, BBBY spent $11.6 billion on share buybacks from 2005 to 2021. Since 2010, BBBY basically burned $9.6 billion in cash on its share buybacks. Like other companies, BBBY used share buybacks to drive up its share price, as “demanded” by its large shareholders and Wall Street. In addition, by not using that money to transition to e-commerce, they began driving the company towards April’s Chapter 11 filing.

A third problem was that the activists that won control of the BBBY board created a self-imposed disaster. While BBBY had withstood competition from Amazon earlier, in 2019, activist investors in control of its board hired a CEO who implemented a private-label product strategy. This led to customers no longer finding the national branded goods they expected on BBBY’s shelves. Products like AllClad, Kitchen Aid, Rowenta, Miele, Corning, Wustof and Braun. So customers bought them elsewhere. That sent sales down even further, and left BBBY in a cash-poor position.

Wrongo and Ms. Right occasionally shopped at our local BBBY stores, both here in CT and earlier in CA. We always thought it was a good value proposition, particularly for towels, sheets and pillows. Back then, the stores seemed well-stocked and the 20% off coupons didn’t hurt.

BBBY followed a classic path to failure: The retail founders preside over rapid growth. Then when Wall Street and the financers get involved, the founders step back. They then hire “professional” CEOs from their big retail rivals who apply whatever worked at their previous employer.

The new leadership skips the crucially important step of giving customers more of what they need than competitors do, focusing instead on sophisticated financial engineering.

All the while their aggressive rivals are going after their customers. This leads to a loss of market share, ultimately sending a once-proud retailing icon into bankruptcy. To BBBY’s credit, they outlasted far older, bigger and better financed competitors from Sears to Montgomery Ward to pretty much everyone else in their household-goods space.

Is late-stage Capitalism at fault in the BBBY story? You betcha.