(Wrongo is back from his project. Regular blogging begins again today.)

In our lifetime, Gross Domestic Product, or GDP, has been transformed from a narrow economic indicator to our universal yardstick of progress. This spells trouble. While economies and cultures measure their performance by it, GDP ignores central facts such as quality, costs, or purpose. It only measures output: more cars, more accidents; more lawyers, more trials; more extraction, and more pollution. All count as success in the GDP equation. In fact, our cumulative real GDP growth since 2008 is 6.9%.

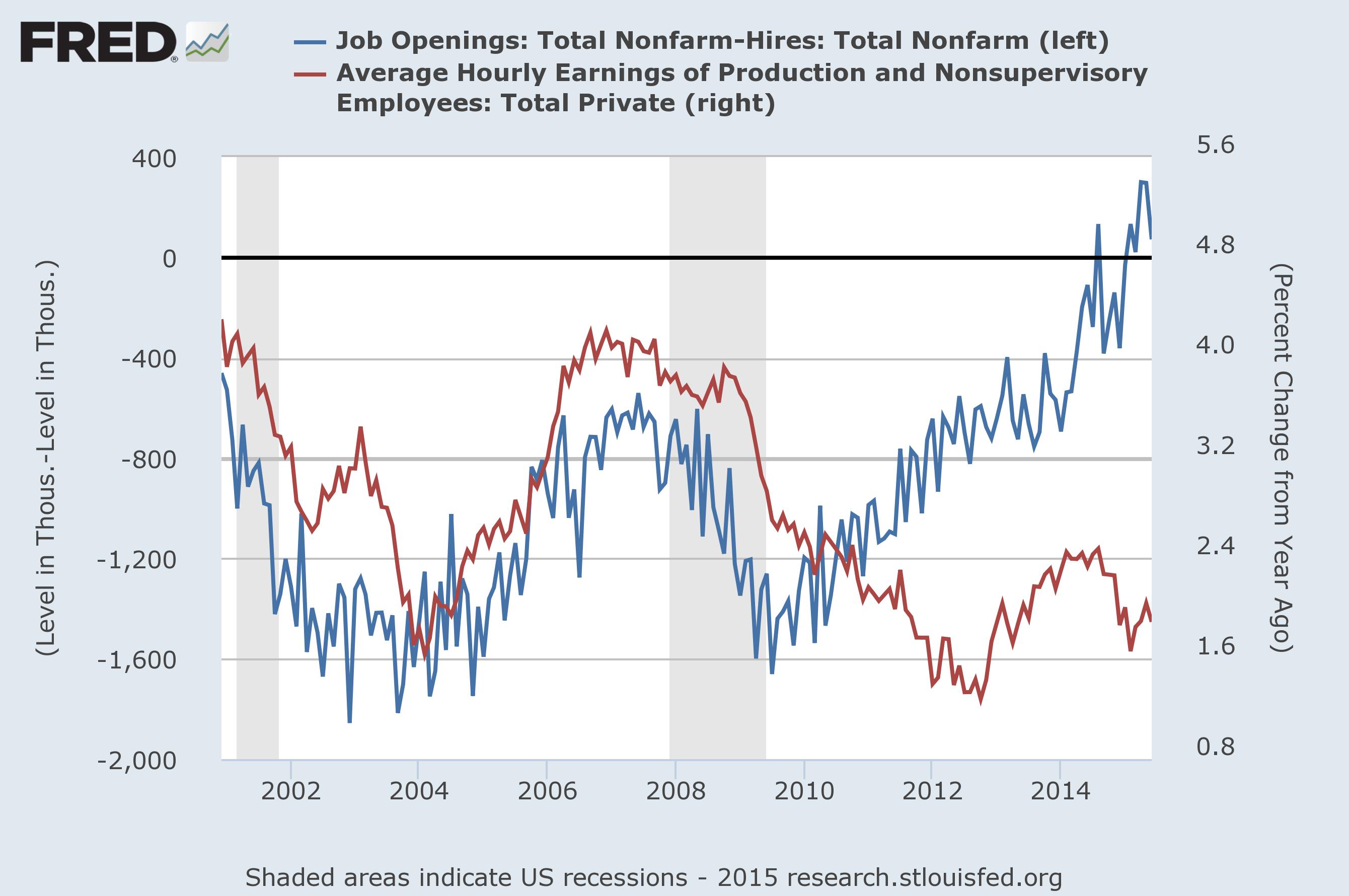

But we need to focus on other yardsticks to understand what is really going on with our economy. First, take a look at the growth in job openings (blue line) vs. growth in hourly wages (red line):

In the past, the two have usually moved in tandem, which makes sense, since the laws of supply and demand should also apply to employment. But since 2011, and most notably in the past year, they have diverged starkly, with wages drifting back to where they were in 2012, while unfilled job openings have skyrocketed: Job openings are now higher than at the height of the tech boom in 2000. And yet, worker’s wages um, suck.

What happened? Perhaps huge numbers of people are now returning to the labor market after years on the sidelines. We know that many people want a job, but stopped searching for lack of opportunities, while many others want more than the part-time work they’ve managed to find. The uneven pace of wage growth shows there is plenty of slack in the labor market. This is supported by Bloomberg’s report that we still need another 2.4 million jobs to reach “full employment”, (5.1%).

So by definition, we can’t be in a tight labor market.

Some of the difficulties driving American job growth are the problems in the global economy. We see low growth in the developed world, coupled with the continuing impact of automation and the movement of much of our remaining manufacturing jobs to low-wage developing nations.

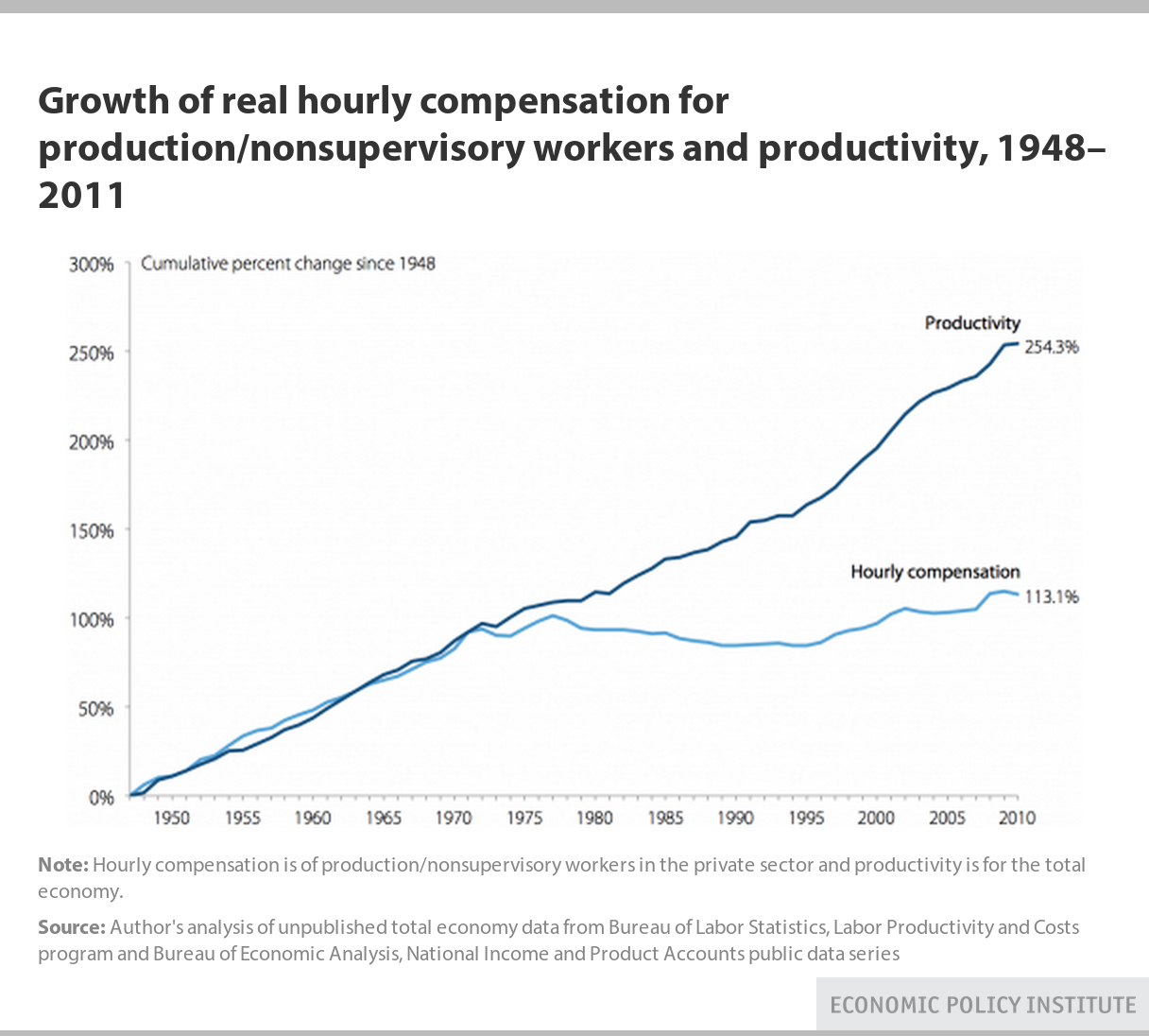

Take a look at another chart, showing the growth in productivity vs. growth in wages:

Hourly compensation grew in tandem with productivity until 1973. After 1973, productivity grew, but the typical worker’s compensation has been relatively stagnant. This divergence of pay and productivity has meant that the majority of workers did not benefit from productivity growth.

This is another way of saying that the economy could afford higher pay, but didn’t provide it.

The analysis confirms that since 1973, the largest factor driving the gap between productivity and median compensation has been the growing inequality of wages. The divergence between wages and productivity we see above, along with increasing concentration of wealth in the very top of the social strata, are not just correlated, they have a causal relationship.

The two charts demonstrate the shift of income from labor to capital. Larry Mishel of EPI notes that from 2000 to 2011, there was a shift from income derived from labor to income derived from capital, accounting for roughly 45% of the gap shown above.

Workers have lost their share of gains in productivity. It was stolen by capital.

Thorsten Veblen distinguished between the Captain of Business, whose focus was on goods production, and the Captain of Finance, who concerned himself with manipulating money. He deplored the replacement of Industry by Finance; and the situation today is far worse than in the early 1900s. (Veblen died in 1929.)

The development of finance since the late 1970s has been near-pathological. It has been essentially unregulated, left free to become an oversized parasite. It has assimilated more and more of our traditional economic activity through “financialization“. The recklessness of that was made clear by its damage to the housing market in 2008, followed by the huge loss of jobs that occurred in its aftermath.

It is that crisis that leaves wages weak today. It is those jobs that we have been looking for the past eight years.

It is well past time to put finance back in its place. The Dodd-Frank law will never be enough, since it continues to allow the very innovations in finance that can take down the financial system, even while pretending to decrease them.

Capitalism has a phenomenal capacity to lift people out of poverty. But it does so at a cost. Capitalism changed before, and it’s time for it to change again. Free markets have existed for thousands of years; capitalism as we now know it, for fewer than 150.

Effective and productive free markets should also provide workers a living wage. If today’s capitalism isn’t the means to that end, it is time to change it.

Glad to see a new post. Since Reagan took office we have had several financial booms and busts… Yet we continue to hear folks who imagine that markets are truly self regulating (and that they solve problems). But as anyone who has studied economics learns, markets do one thing – solve for price, which can be made to sound like fairly allocates goods, but the allocations are not fair. Nor is the selection of good fair. If we let the markets run wild, everything will become like food in the chip aisle in the grocery store (so really garbage).

Conservatives make a lot of noise over the mistakes that happen when govt intervenes in markets, but they never admit to the mistakes when govt leaves markets alone. If solyndra is an example of a govt intervention that did not bear fruit, we need to counter that against the collapse in 2007-08.