The auto industry has had a spectacular run since we bailed them out in 2009. We saved it because the auto industry is crucial to the US economy and jobs. Auto sales have accounted for 21% of total retail sales so far in 2016.

The trickle-down effect is huge, from transporting new cars via truck and rail to financing and insuring them, and collecting the tax revenue they generate for state and local governments, sales of cars generate lots of jobs and money for our economy.

But the seven-year boom may be near its top.

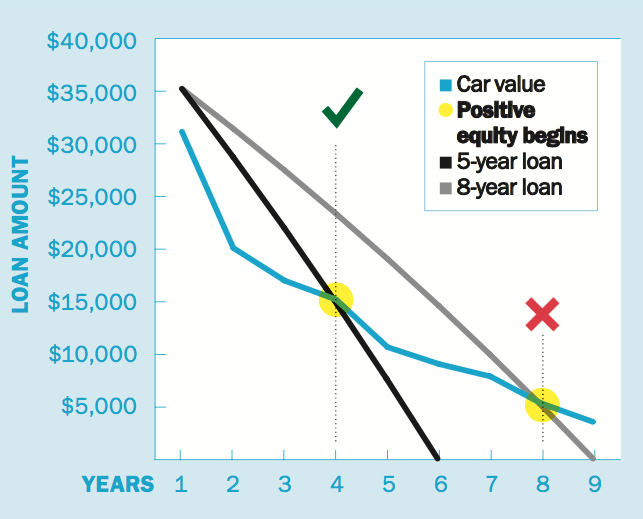

Take underwater car loans: Bill wants to buy a new car. His current car has a trade-in value of $20,000. But he owes $25,000 on it because when he bought it new a few years ago, he financed it for 84 months to keep the monthly payment low. He also asked the dealer to roll the amount for tag, title, and license fees into the loan, along with the $2,000 he was upside down on his trade. So he buys a new $30,000 car that now costs $35,000. He may consider financing this with car title loans near me, or he may have other options he can take.

The car is financed with a 4% interest rate loan. If Bill took a five year loan, he would start accumulating positive equity-where the car’s market value becomes greater than its loan balance-midway in the fourth year. However, there are loans that might be able to help for example those that are similar to Ikano Bank VISA as well as looking loans before they take them out. If he took an eight year loan instead, he would be $9000 underwater at the same time, and won’t start accumulating any positive equity until the end of the seventh year:

Source: Money Sense

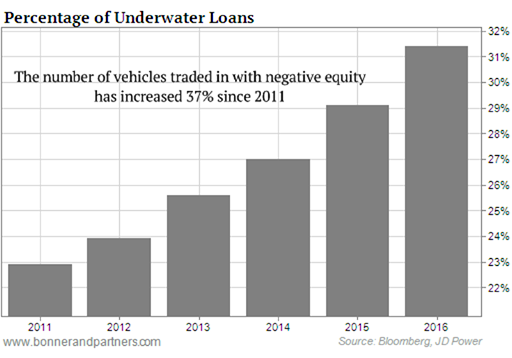

So just how big is the problem of negative equity? Since 2011, the number of vehicles traded in with negative equity has ballooned by 37%, and underwater auto loans now account for a record 31% of all vehicles traded in:

(Chart by Chad Champion, at Bonner & Partners):

One reason negative equity is rising is that lenders have extended the duration of car loans to keep monthly payments affordable. If a customer has a lower monthly payment, she/he’s likely to owe more than the vehicle is worth for a longer period. Bloomberg reported that the percentage of car loans that are longer than six years was 29% in 2015, up from just 9.6% in 2010.

Growth in loans to subprime borrowers is also driving growth in auto sales. Experian Automotive reported last month that poor credit consumers (subprime) now make up a record 20.8% of the new auto loan market – more than one in five new auto loans are going to subprime borrowers. We remember subprime from the housing fiasco of 2008. Subprime is back, but not yet causing alarm bells to ring.

Subprime borrowers pay higher rates: Average rates for subprime loans were 10.36% in the fourth quarter of 2015 while the poorest subprime borrowers averaged 13.31%. At the same time, new car buyers with excellent credit paid 2.7% interest.

The Office of the Comptroller of the Currency has noticed the problem. In its most recent Semiannual Risk Perspective, the banking regulator warned: (emphasis by the Wrongologist)

Underwriting practices and weak loan structures in auto lending are most concerning in banks with high concentrations to try Auto Finance Online. Strong auto loan growth alone does not pose systemic risk…Even as banks have increased capital levels, auto loan portfolios represent greater than 25% of capital at about 15% of banks.

The OCC worries that the rapid growth of auto loan balances are not a problem per se, but the “extended durations of loans caused by lengthening maturity schedules” and the rising loan-to-value ratios are a concern. Together, they “create a longer period of time that banks and consumers are in a negative equity position.”

This is what happens when the players in the auto sales game, both the manufacturers and financiers game the system to front-load sales and profits, thus paving the way for an eventual reckoning.

And here is the other issue: When we export manufacturing jobs to places such as Mexico (who now manufactures for Ford, Chrysler, GM, VW, Toyota, Nissan, Mazda, and Honda and exports 70% of the cars it manufactures to the US), we lose the purchasing power of all those people who used to have jobs in the US auto industry. So corporate America’s solution is to make credit cheap and easy so that working stiffs can leverage themselves even more in order to buy a new car. Obviously, some loans are needed at certain times in peoples lives, if you are looking at how to get a loan there are many websites that can give you a guide.

To be sure, the car buyers are culpable, but the system relies on foolish people to go deeper into debt in order to fuel the system.

Impressive boom to possible bust ? this show is brought to you by corporate America, with support from the Federal Reserve.

Wrongo,

When I read your posts about the current financial state of this country, I have a burning urge to buy gold and hoard seeds. Is it really that bad or am I overreacting?