The Daily Escape:

Death Valley dunes, CA – August 2022 photo by George Cannon

At a dinner party over the weekend, blog reader Marie S. said that she felt ambivalent about Biden’s loan forgiveness plan. Several others (some were Democrats) echoed her viewpoint.

Republicans have attacked it because they’re desperate to change the subject from the extremist abortion position that they’re now trying to rapidly back away from. They’re also desperate to keep Trump off of the front page. With the loan forgiveness, they see an opportunity to excite their base and divide the Dems.

Wrongo agrees that there are things to dislike and also things to like about the plan. The major thing not to like is something that the Biden administration isn’t in a position to control: The high cost of higher education. Many say that it will be business as usual for our colleges and universities, with loan forgiveness needing to happen every ten years or so.

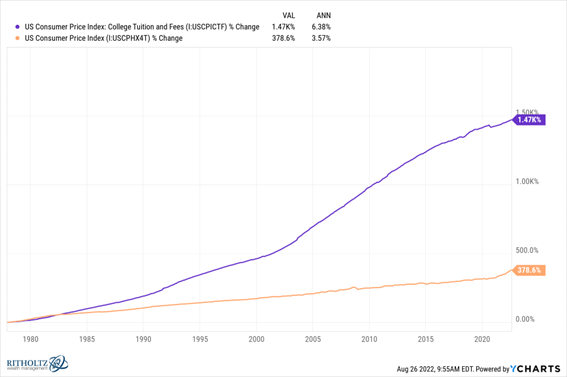

The cost of higher education is out of hand when we look at the growth in the cost of college and fees compared to the US consumer price index (CPI):

The chart shows that the cost of college is up exponentially more than CPI over the past 40+ years. For any child not born to affluent parents (or getting a hefty scholarship), the choice is foregoing college or taking on a ton of student debt.

Dealing with the increase in college costs isn’t something that the US government can do easily, if at all. We’re talking about a broad spectrum of privately owned institutions and an array of institutions owned by individual states. Biden has got zero power to flatten the cost curve.

Also, nothing is being demanded of the banks who made questionable student loans or the schools who gave students unrealistic information about their future earnings prospects, inducing them to commit to school.

One change that Biden could have made would be to make student loans dischargeable in bankruptcy, as they were before the 2005 bankruptcy “reform” that then-Senator Biden helped push through Congress.

Businesses that make bad decisions get to restructure their debts and carry on. Individuals who have a run of bad luck (big medical bills or job loss) can file for bankruptcy, but students cannot. Why should college debt be carved out as not dischargeable in bankruptcy?

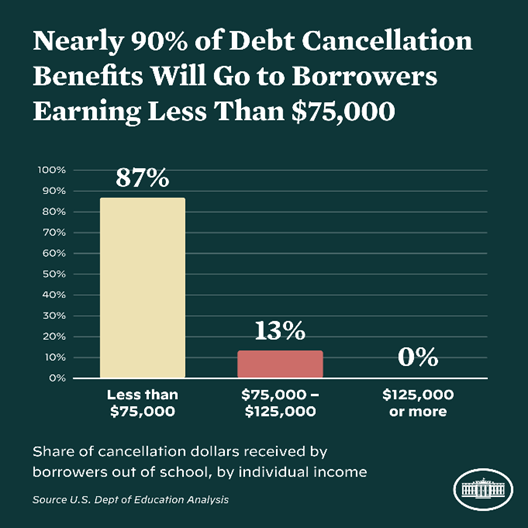

The program’s means-testing could have been tighter. The $125k (individual) and $250k (for married couples) income caps do seem high considering those levels of earnings puts you in the 76th and 94th percentile of earners respectively. OTOH, it sounds worse than it truly is. See this chart:

Wrongo also doesn’t like the fact that the government is still charging high interest rates on student loan debt. The average interest rate for existing borrowers under the program is 5.8%. A 5.8% interest rate on the $1.6 trillion of outstanding student debt equates to $93 billion a year in interest payments if all of those people were paying back their loans. Much of that big number could stay in borrowers’ pockets at a lower interest rate.

Finally, the US government owns 92% of all student loan debt. Why does the government need to make so much money on this debt? Wouldn’t a lower rate be a good investment to make for future generations of workers?

Wrongo does like that younger people are finally being helped out by our government. Pundits complain young people don’t get out and vote. Maybe that’s because politicians don’t help young people enough.

It feels like the government has ignored people under 40 in favor of the Boomers and corporations. Today’s young people have much higher costs for essentials: Their student loans, daycare, healthcare, their cost of housing, all are much more than previous generations had to deal with.

Wrongo does like the possible psychological benefit this could give people who felt like they were stuck. The White House estimates that more than 43 million people will qualify for loan forgiveness. Wrongo thinks that the majority of these 40+ million people are overjoyed by this news. His narrow survey of college age grandchildren shows them to be deliriously happy.

And most borrowers will likely experience some psychological relief along with their financial relief. It may allow some people to buy a home sooner than expected. Or get married or start a business. Or just stress a little less about money.

On balance, given the good and the not-so-good, Wrongo thinks the program is a good idea.

In the meantime, the politics bear watching. Republicans are trying to stoke jealousy, and they might succeed. Republicans don’t agree that this relief should take place. But every complaint makes it clear why Biden was right to do this.

Before Reagan on average states funded 75% of college costs. The decline started as an side effect of Reaganism such that now state schools receive only 25% of their funds from the state. The shift not only forced borrowing, but it also made formerly sleepy state schools (like Montclair State Teacher College as it was once known), to change their look and feel to attract the paying customer. I grew up near the college on a street where many profs lived.

So these once humble colleges have much more elegant dorms, fancier gyms etc. All to attract the out of state and overseas student. (Even in the 60s and 70s Montclair had Iranians and other foreigners in respectable bundles).

Reversing the trend will be very difficult.