The Daily Escape:

First snow, Doubling Point Lighthouse, Kennebec River, ME – December 2023 photo by Rick Berk Photography

Wrongo may have stumbled upon the reason why people say the economy is bad when so many economists say it isn’t. From a LendingClub report from last May: (emphasis by Wrongo)

“For some Americans, earning a six-figure income doesn’t guarantee a comfortable lifestyle….many Americans are struggling to make ends meet — with 61% of those surveyed saying they feel stretched too thin, and 49% of those earning $100,000 or more saying they’re living paycheck to paycheck.”

This ties together with other information, some of which comes from the issue, who reported this from the Aspen Institute: (emphasis by Wrongo)

“Though routinely positive cash flow is the starting point for financial stability, it remains largely out of reach for many Americans. Even before the fallout of the COVID-19 pandemic, nearly half (46.5%) of households reported that their income did not exceed their spending over the course of a year. For households with annual income of less than $30,000, this number increases to three in five (61.5%).”

Now there may be many reasons why people spend beyond their means. Some seem to be unable to defer gratification until there’s money in the bank, so they buy on credit. There was a $48.5 billion jump in spending from September to October 2023. For others who make less than a living wage, the problem isn’t one of choice, it’s existential.

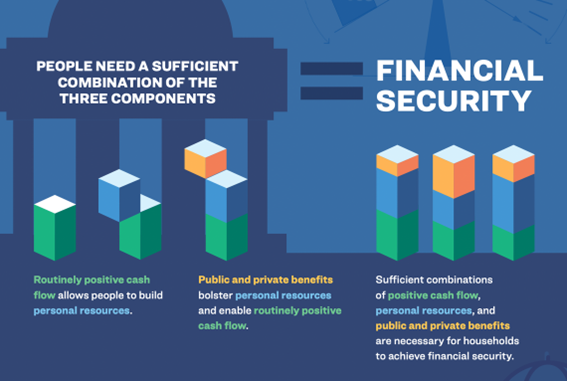

The searing takeaway from the above is that negative personal cashflow was a problem even before the post-Covid inflation drove prices through the roof in America. The Aspen Institute provides this handy chart showing how individuals build financial security:

Financial security starts with having a routinely positive cashflow. But, nearly 50% of Americans today aren’t cash flow positive (see quote above), while 49% of people earning more than $100k are living paycheck to paycheck.

This dovetails with Wrongo’s Monday column which showed that “Nearly 3 in 10 Americans say they have had to forgo seeing a doctor in the past year due to costs.” If you’re one of the 7.5% of uninsured Americans, and have money in your checking account that isn’t going to necessities, you can definitely go to the doctor.

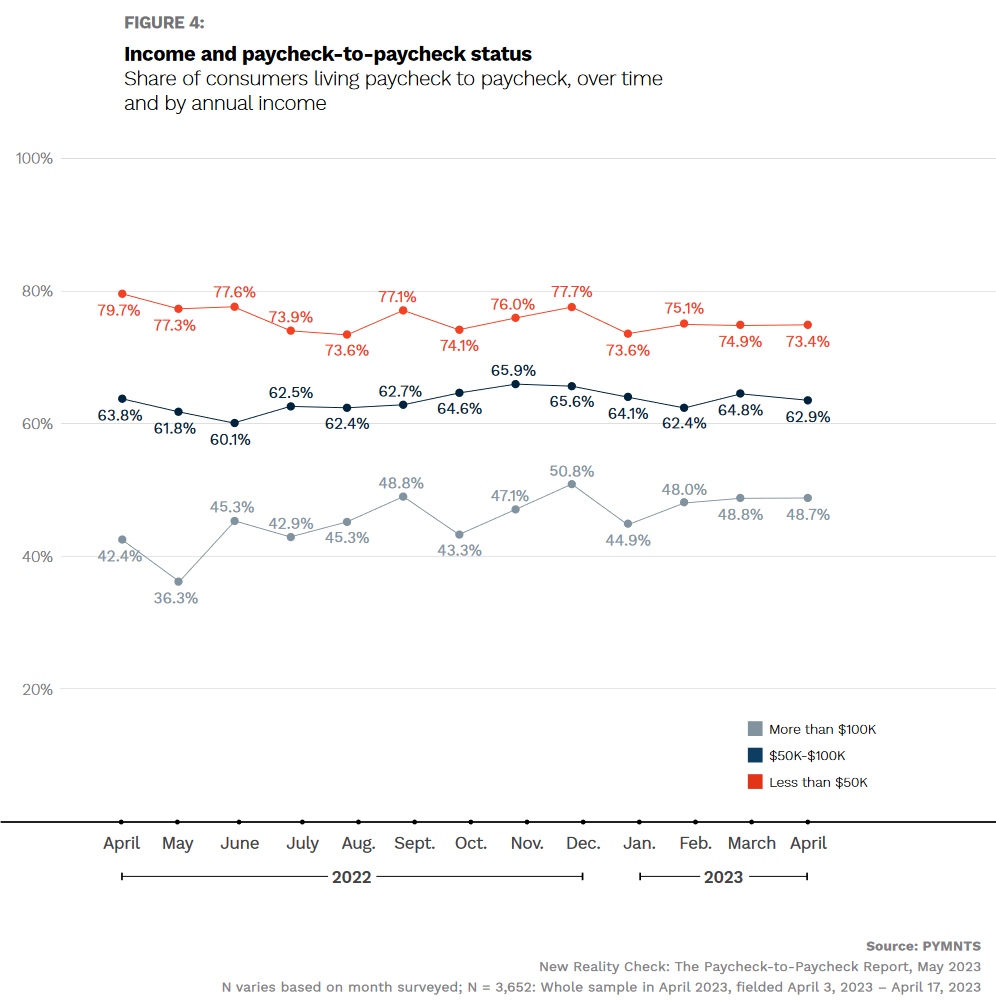

Aspen has another chart that shows the breakdown of who lives paycheck to paycheck by income levels:

Seventy-four percent of those making less than $50k are living paycheck to paycheck, and while the percentage gets smaller as annual income rises, it’s still 48.7% for people making more than $100k, in an economy where the median income is around $54K! FYI, the percentage of Americans who make $50k or less is 37.8%.

More from LendingClub: (brackets and emphasis by Wrongo)

“The share of consumers in the US earning over $100,000 per year who live paycheck to paycheck increased 7 percentage points in April year over year. High-income consumers are particularly likely to live in urban areas, at 36%, and these tendencies toward higher incomes…[don’t] prevent almost 70% of urban dwellers from saying they live paycheck to paycheck.”

It’s hard not to conclude that the majority of Americans are currently experiencing dire financial conditions, including many who live with negative cashflow. When your cashflow is negative, you either cut back, borrow or sell assets. For most people selling assets isn’t a real choice. So while some cut back, the majority borrow to make ends meet. According to the issue, the:

“…highest risk, and most expensive forms of debt are now growing fastest. Payday loans, online insta-loans, and so forth. That means that people are exhausting the more mundane forms of debt—credit cards, bank loans, government loans, etcetera.”

This squares with a report by Achieve, a personal debt management firm, that shows:

“In the first nine months of 2023, the average monthly participation in debt resolution programs increased by 119% compared to 2020, even though the average earnings rose by approximately 37% during the same period.”

It gets worse:

“In 2023, the typical household income of individuals enrolled in debt resolution programs was $59,900, which is a notable increase from $43,598 three years prior.”

Americans are earning 37% more but are still struggling with debt. Not a pretty picture to take before the voters.

Meanwhile, Democrats still are touting how “strong” the economy is. The aggregate numbers hide terrible personal experiences that are happening out of sight of our politicians and surprisingly, our economists. However, it’s clear from the polls that few Americans are buying that message apart from the true believers, the media and pundits.

The disconnect between economic data and the lived experience of average people needs to be addressed by Biden and the Democrats. If nothing is done to at least acknowledge the actual problems of many Americans specifically, their negative personal cashflow, these angry folks will certainly tilt toward giving Trump another chance.

Let’s give the issue the last word:

“What is this? What do we call it when the majority of people can’t make ends meet, as in, they’re literally spending more than they make, because they don’t make enough to live a stable or secure life?

Today the averages are hiding a truth: that a near-majority of American citizens are financially underwater. These are big numbers. The Census Bureau says as of now, 258.3 million Americans are adults. And the Aspen Institute says that 46.5% of them can’t make ends meet. That’s 120 million of us that are going deeper in debt every month.

That can only happen when those at the very top are skimming off more than 100% of the growth in the economy. This suggests that Biden et al need to run on policy that will help the majority of voters, not simply the moneyed people who finance political campaigns.

Ouch! This strongly suggests that I am out of touch with the lived experience of a huge segment of the population

I was very penurious during the years while a student (including 3 while a parent of young children). I notice that similarly positioned young adults that I know seem to live beyond their means in ways that I did not My girlfriend/wife and I did not eat in restaurants or take trips or have late model cars We grabbed whatever part time jobs we could and generally pinched pennies I am sure there are plenty of young people who do as I did back then But I see at least some who don’t think they should have to