The Daily Escape:

Wrongo’s calendar says there’s just 29 days to go until Election Day. The campaigns are in high gear, but what are they saying? And is what they’re saying getting through to both their base voters as well as to those who are “persuadable” enough for them to get out to the polls and vote? Time is running out.

Timing is a point raised in this NBC story, which describes that, after having taken the last 76 days to introduce the Vice President to voters, the campaign now plans to ratchet up negative advertising about how unfit Trump is to be President (emphasis by Wrongo).

“Leaning more heavily into negative campaigning is a strategic shift for Harris. While she has routinely been critical of Trump since becoming a candidate in July….Harris campaign officials said they intend to continue laying out her policy positions, background and plans…But emphasizing what Harris campaign officials view as Trump’s major vulnerabilities is seen as possibly one of the only ways to finally win over some voters who haven’t made up their mind in a static race that Democrats want to push in their direction.”

A recent poll by the Associated Press-NORC Center for Public Affairs suggests that Harris’ attacks on Trump’s brand of hyper-masculinity appear to be working. As the Daily Beast summarized the findings, respondents:

“…chose Harris 59% over Trump’s 57% when it came to which candidate they felt was tough enough to be president…and favored Harris 55 to 46 % on “which candidate would change the country for the better,” and by 54 to 43% on who “was more likely to fight for them.”

Harris also is micro targeting the message of Trump’s weakness. From the WaPo:

“For the millions of football fans who tuned in from home for Saturday night’s much anticipated matchup between the University of Georgia and the University of Alabama, she also ran a new ad nationally on ABC that hammers home her point.”

The ad says:

“’Winners never back down from a challenge. Champions know it’s anytime, anyplace. But losers, they whine and waffle and take their ball home,’ the narrator says at the start of the spot, over images of a football game and washed-out footage of Trump missing a golf putt. The 30-second ad ends with footage of Harris challenging him to another debate, with the words “When we fight, we win” hanging on a sign in the background.”

The money quote:

“Well, Donald, I do hope you’ll reconsider to meet me on the debate stage. If you’ve got something to say, say it to my face,…

Harris also posted the ad on Trump’s Truth Social media platform.

Marcy Wheeler quotes CNN’s David Wright who tracks political spending by the candidates about where the money is headed in this final month as the ad wars intensify:

“You can see how each side is placing bets on their best path to 270 electoral votes. In the first week of October, the Harris campaign is spending the most in the critical trio of “Blue Wall” states – they’ve got more than $5 million booked in Pennsylvania, about $4 million booked in Michigan, plus about $2.7 million booked in Wisconsin. And that makes sense – if Harris wins all three of those states, plus Nebraska’s up-for-grabs electoral vote in the swingy second congressional district (where the campaign also has more than $300,000 in ad time this week), she’s the next president.”

Turning to Trump:

“…he’ s looking to the Sun Belt. This week, Trump’s campaign is spending the most on ads in Pennsylvania, $3.8 million – it’s really the linchpin to both sides’ strategies. But in addition to that, the campaign is also spending $3.4 million in North Carolina and nearly $3 million in Georgia, its other top targets, and if he wins those two states plus Pennsylvania, he’s heading back to the White House.”

The Electoral College will come down to which of the two campaigns potential voters consider more trustable, probably mostly on their personal economic situation and where that’s heading with each potential president. From the WaPo:

“Americans are finally starting to feel better about the economy, invigorating Vice President Kamala Harris’s pitch for the presidency as she narrows her Republican opponent’s longtime lead on an issue that is foremost on voters’ minds.”

More:

“Although voters still favor former president Trump over Harris on handling the economy, his advantage has dropped dramatically in recent weeks. Trump now averages a six-percentage-point edge on the economy…”

But Trump’s only answers for the economy are lower taxes on the rich and more tariffs. Yet, like everything else, Trump has no idea what tariffs actually do.

However, a new survey by Data For Progress’s top line finds Harris leading Trump by 3 points among likely voters nationwide. Nearly half of voters (49%), including a plurality of Independents (46%), choose Harris, while 46% choose Trump.

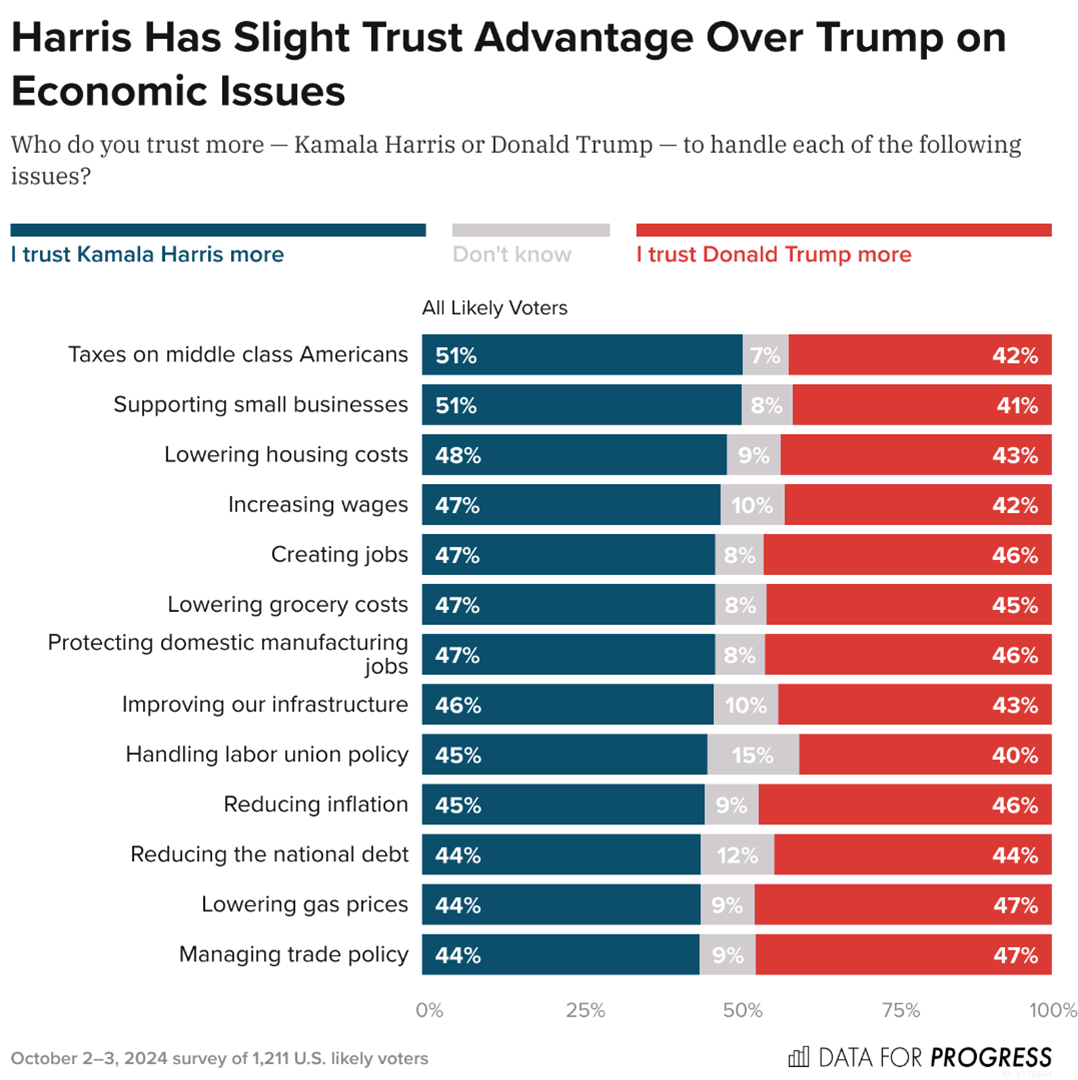

On the all-important economy, Harris has a trust advantage on most of the economic measures tested, including: supporting small businesses (+10 points), taxes on middle class Americans (+9), increasing wages (+5), lowering housing costs (+5), handling labor union policy (5%), improving our infrastructure (+3), lowering grocery costs (+2), creating jobs (+1), and protecting domestic manufacturing jobs (+1).

That says her campaign messaging is getting through.

Also the survey finds Trump with just a +1-point trust advantage over Harris on “reducing inflation,” an issue that voters have consistently ranked as their most important when deciding whom to vote for. Here’s their chart:

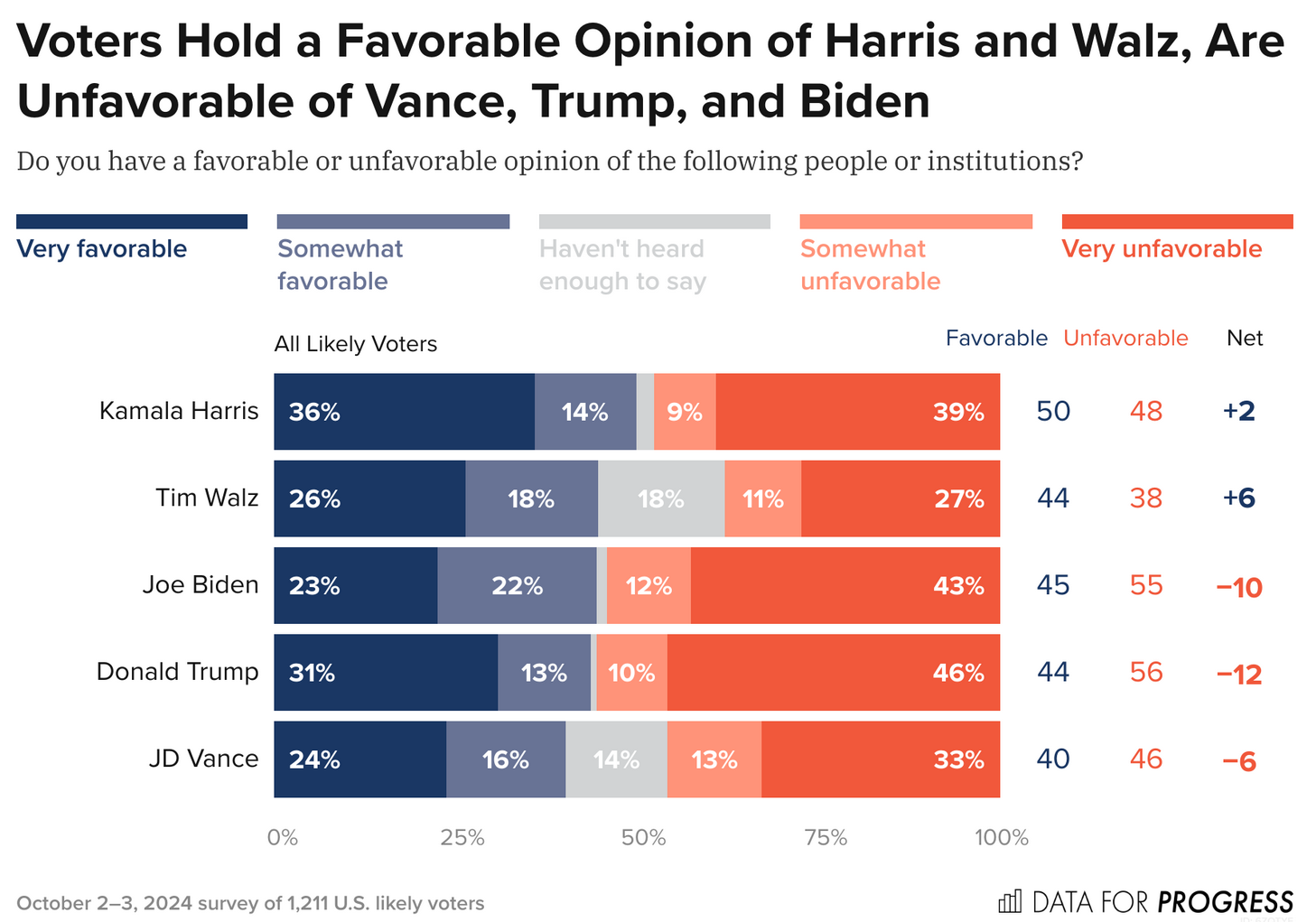

They also surveyed candidate favorability, which now tilts towards Harris. Harris’ rating is +2, while Trump’s is -12:

Is this poll on the money? Difficult to tell. A shorter election season makes it harder for campaigns to assess where to place their bets. And which of their cohorts in the electorate demand the most attention. We’ve focused on Gen Z and younger voters as being primarily swayed by economics. Messaging to women is another important element. Harris can run ads attacking Trump’s hyper-masculinity, (which will help with women).

From The Economist: (emphasis by Wrongo)

“And Harris needs to focus there. In the Obama years the gap between young men and women identifying as liberals was just five percentage points, during the Trump-Biden years this has tripled to 15 points, according to Gallup. This change has been caused almost entirely by young women moving to the left, rather than young men tacking to the right. The fact that this generation’s formative years were during the #MeToo movement, the Trump years and the decision to overturn Roe v Wade helps explain it.”

In 2020 a majority of white women voted for Trump. He will be in the minority in 2024. Leading among women is a real advantage. Since the 1980s a greater share of women than men has turned out to vote. In 2020 women made up 54% of the electorate. A final indicator that Democrats might be winning this battle of the sexes: in battleground states, according to Target Smart, a data firm, between July and September, twice as many young Democratic women registered to vote than young Republican men.

Trump’s bet is that Harris is the one with the turnout problem. They think their base is more committed to their candidate than is Harris’s. But Marcy Wheeler points to Harris’s investment in the Dem ground game:

“The Harris campaign claimed in late September to have 330 offices and more than 2,400 staff. They completed 25,000 weekend volunteer shifts on the final weekend of last month, contacting over 1 million voters over three days and completed the 100,000th event of the campaign.”

BTW: Ms. Oh So Right got a postcard from Harris to vote early this week.