The Daily Escape:

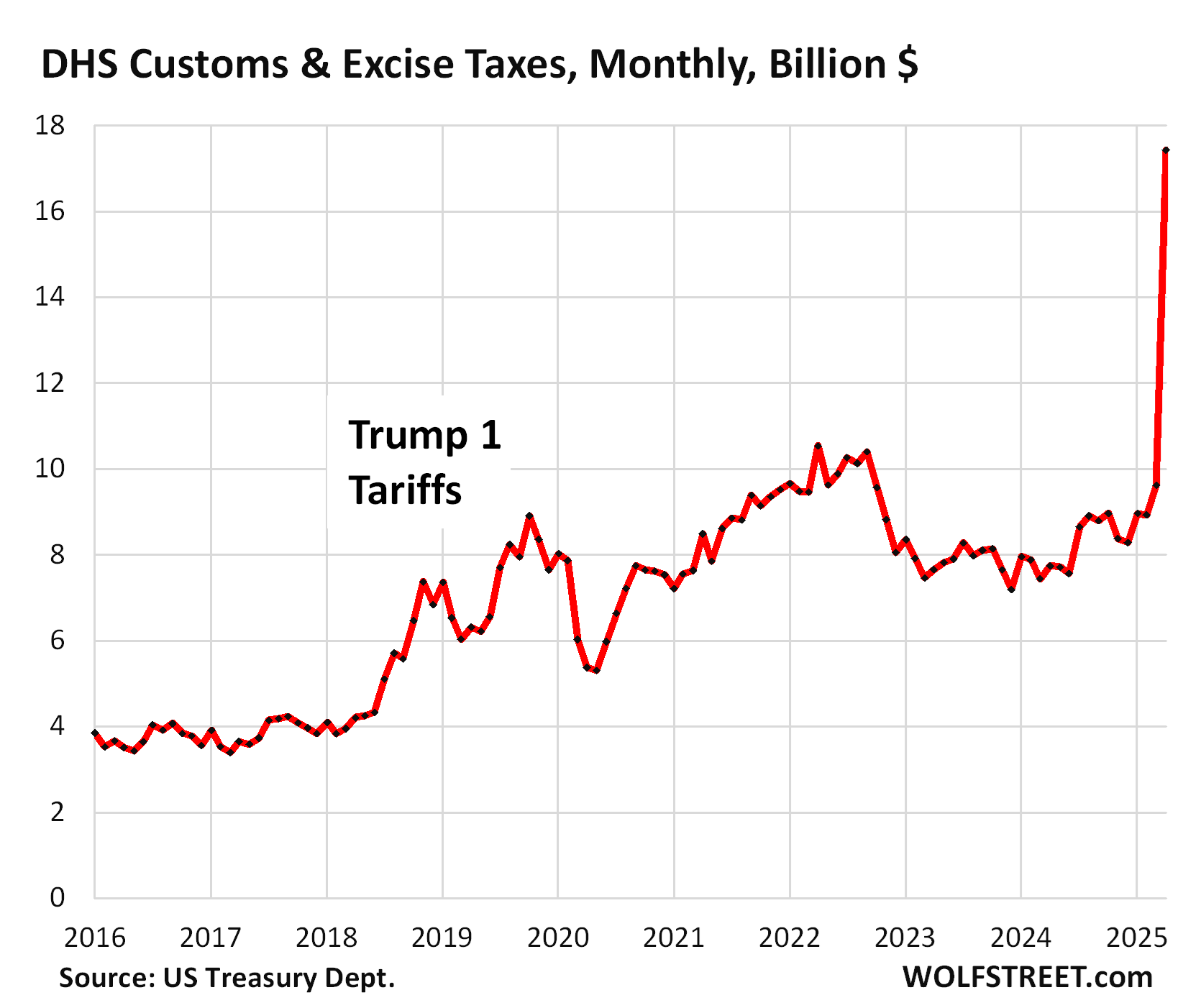

The cash flow of Customs and Excise Taxes has doubled in the past two months. From Wolf Street:

“Collections from customs and excise taxes spiked by 81% in April from March, to $17.4 billion, more than double the average monthly collections in 2023 and 2024, according to Treasury Department data today.”

This is the amount in customs and excise taxes that the Department of Homeland Security (which includes Customs and Border Protection) transferred in April into Treasury’s checking account at the Fed. Here’s a graphic representation:

The chart shows that something substantive is starting to happen. Tariffs are taxes paid by businesses to our government. And it adds up:

“For example, GM just announced that the new tariffs would cost it $4 billion to $5 billion this year and lowered its earnings forecast with respect to that. It has also begun to shift production to the US to dodge some of those tariffs.

GM manufactures components in China, it manufactures its Buick Envision at its joint venture in China and imports it, it imports vehicles and components from Mexico and Canada, it imports components and materials from around the world. After its bailout out of bankruptcy by the US government in 2009, GM focused on China and Mexico and shed dozens of US production facilities for components and vehicles. So now there’s a price to pay.”

Today’s automobile market is such that GM cannot pass on these tariffs to consumers. Automakers are having to discount their models and provide incentives to the market to sell enough vehicles to keep their production lines going.

More from Wolf:

“After the massive price hikes during the pandemic, there is no more room left to hike prices. Consumers have had it.”

But profit margins in the auto industry were huge following those massive price hikes. And the companies can eat those tariffs, show up with lower profits, and still be fine.

And not just in the auto industry. Non financial companies in the US made out like bandits during the Covid era of massive price increases. Their balance sheets have plenty of room to absorb the tariffs.

Mere mortals like Wrongo can’t keep up with all the tariff chaos. The governments of China and US are at least now talking about talking about tariffs. Numerous negotiations are apparently underway with governments of other countries, each one trying to get their special deal with Trump.

Under the Biden administration, there were numerous announcements of large investments in US manufacturing facilities by manufacturers. These investments will take time to play out: Years of big investments in the US before mass production can start. These investments alone are a big boost for the US economy. And companies such as GM that already have plants in the US have started to shift more production from their foreign plants to the US plants.

Trump has misplayed his own China tariffs strategy. In 2024 he said that if China tried to invade Taiwan he would impose tariffs:

“I’m going to tax you, at 150% to 200%.”

But today he already has tariffs at 145%. A trade war is about who can take the most economic pain, and that is a fight China clearly thinks it can win.

Trump’s trade protectionism is also harming America’s allies. Trump is pressing Taiwan and others to shift plants to America. Australia, Japan and South Korea face tariffs and demands to decouple from China, a large trading partner for each.

While no Asian country is about to break its security alliance with America. However, countries will be even more queasy about being dragged into a fight over Taiwan.

Trump’s problem is twofold. First, people are smarter than he thinks. They know the economy has worsened since the chaos of Liberation Day. They can see the demarcation in time when the vibes shifted. Second, of all the insanity of the first 100 days of Trump, nothing broke through to the broader public besides tariffs.

From the NYT:

“By late May or early June, consumers could start to see some empty shelves, and layoffs could occur for retailers and logistics industries. The major effects on the US economy of shutting down trade with China will start to become apparent in the summer of 2025…”

Trump desperately wants to evade blame. People have soured on his economic leadership devastatingly early into his presidency. It puts his power — and the Republican majorities’ power — at risk. Trump is very good at getting out of messes. But can he escape this one?

The stated dual purpose of tariffs is to first, change the math for manufacturing in the US. That was already underway with Biden. Second, to increase tax revenues.

Tariffs were the original tax revenues in the US, predating income taxes. And Trump mistakenly wants to take us back to that.

Suck it up, buttercup:

Suck it up, buttercup: