The Daily Escape:

Super moon over Lake Champlain, Burlington, VT – August 2022 photo by Adam Silverman Photography

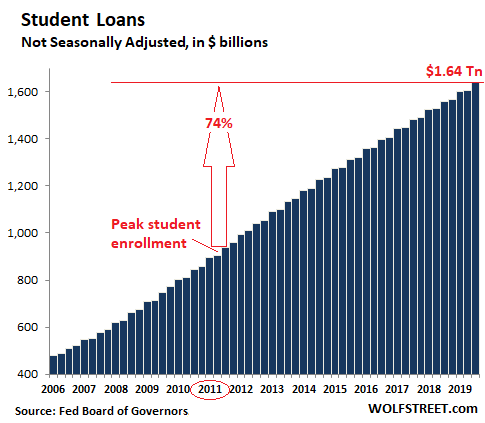

Republicans are outraged this week about Biden’s cancellation of student loan debt! Americans now owe a total of more than $1.6 trillion for higher education. From the WaPo: (emphasis by Wrongo)

“The result is one of the most significant changes to American higher education policy in decades — and a new cornerstone of the president’s economic legacy. Biden’s decision will dramatically change the financial circumstances of tens of millions of Americans, fully erasing the student loans of roughly 20 million people.”

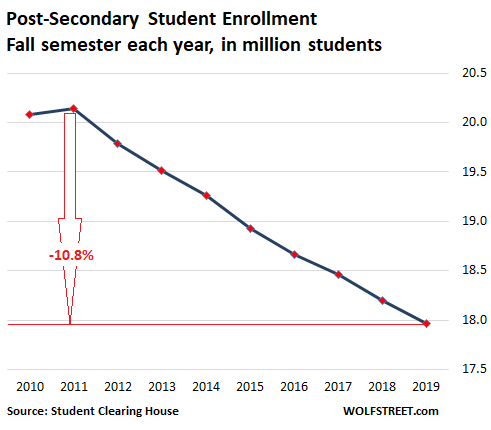

Student debt played a minor role in American life through the 1960s when Wrongo accrued his $5k of college debt while attending Georgetown. But it increased during the Reagan administration. It then shot up after the 2007-2009 Great Recession as states made huge cuts to funding for their college systems.

But the argument that “tuition has gone up because public support for higher education has declined” isn’t the only one. While it’s valid for some institutions, it doesn’t explain the “arms race” among colleges and universities to add student amenities and layers of administrative staff over the past 10 years.

Over the last decade, revenue at independent (non-religious) private colleges and universities in the US has increased by 148% on an inflation-adjusted (real) per student basis. At religiously affiliated private colleges and universities revenue has increased by 87% in real per-student terms over the last 10 years.

Meanwhile, at public institutions, revenue has increased by just 23.4% on the same basis. However, this is still 36% greater than per capita GDP growth over the same 10 years.

The headline is that our elite educational institutions have gotten obscenely wealthy. And many of our second tier institutions chased after them, causing education budgets everywhere to explode.

It’s become another example of America’s new gilded age.

Opinions differ about the ethics of loan forgiveness for student debt, and that’s understandable. The general thrust of the Republican railing about the educational loan forgiveness is about how unfair it is when one group of Americans is getting a benefit at the cost of other Americans.

This tweet from former Trump White House press secretary Sarah Huckabee Sanders is on point for most of the GOP:

“Joe Biden wants those who didn’t go to school, didn’t take out loans, or already paid off their loans to pay off $300 billion of other people’s debts…..It’s socialism, it’s un-American, and only makes his record-setting inflation worse.”

But it isn’t socialism when our government bails out one group at the expense of another; it happens all the time. No Republican complained about the Trump tax cuts which were directed at America’s wealthy and its corporations. No Republican complained about the bank bailout in 2008. No Republican objected when Trump gave $16 billion to farmers hurt by the Trump tariffs.

Second, despite what the GOP is saying, the $300 billion in loan forgiveness isn’t inflationary. It’s true that it’s money that student borrowers won’t be paying back. But because of the student debt moratorium, they had already stopped payments in 2020, so there’s no change going forward. They simply won’t have to restart making payments on that $10,000 of debt.

It isn’t clear that there will be much impact to inflation or the Consumer Price Index. Since they weren’t making payments, it’s likely they were already spending those funds that might have gone to loan repayments. So no new spending.

We can have a debate about how much higher education should cost per student. We live in a society that is a whole lot wealthier than it was 40 years ago, but many of our students do not come from those few wealthy families.

The political calculus of Biden’s decision will be seen in November. The WaPo reported that a majority of Americans support limited debt forgiveness. Biden’s pollster, John Anzalone said:

“This is a motivator for young people….It’s a huge issue for young people — the support levels for them are in the high 60s.”

Let’s hope they turn out to vote on November 8.

Now, it’s time for our Saturday Soother, where we decompress from another week of body blows to America and find a few moments to gather ourselves for the week to come.

Here on the Fields of Wrong, we had a day of very satisfying brush clearing although we’re still waiting for rain.

Go get a big mug of decaf cold brew coffee and grab a chair in the shade. Now listen to Schubert’s “Impromptu in G flat Op. 90 No. 3”, written in 1827, and played here in 2012 by Olga Jegunova at the Bishopsgate Institute in London:

Schubert really understood how to capture emotion in his music.