(Email publishing of The Wrongologist should be restored as Wrongo is using a different vendor, WordPress. Apologies to those who read in email.)

The Daily Escape:

Cliff Palace, Mesa Verde National Park, Colorado, as it might have looked at night in the 12th Century lit by camp fires. Mesa Verde is unique since it is the only NP that preserves the works of man – photo by Rick Dunnahoo

This is going to be a historic year, even when compared to 2018. And it’s starting out with a bang. The government is shut down, half the cabinet is empty, the 2020 presidential race has officially started, and the Democrats are taken over the House.

And that’s without whatever Mueller shoe will drop sometime in the year, or whatever Twitter atrocities Trump decides to commit. In other words, we’re going to have our hands full.

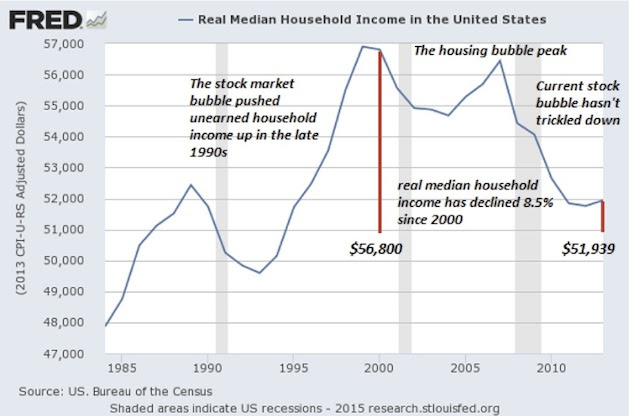

But today, let’s talk about how bad the economy is below the surface of the headline numbers. Debt is rising, and rising debt is supposed to be matched by rising income. It shouldn’t be a surprise that more income is required in order to service more debt. But so far, in the 21st century, for the bottom 90%, debt is growing while income is stagnating.

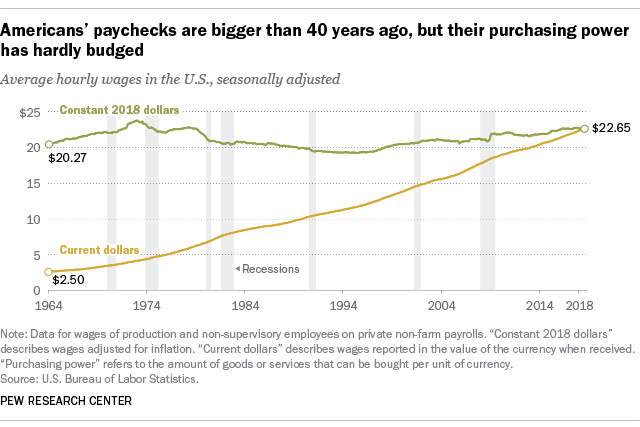

Pew’s Fact Tank has an analysis that speaks to this problem. Average hourly earnings for non-management private-sector workers in July were $22.65, 2.7% above the average wage from a year earlier. But in the years just before the 2007-08 financial collapse, average hourly earnings often increased by around 4% year-over-year.

And during the high-inflation years of the 1970s and early 1980s, average wages commonly jumped 7%, 8% or even 9% year-over-year.

However, after adjusting for inflation, today’s average hourly wage has about the same purchasing power it did in 1978. In fact, in real terms average hourly earnings peaked more than 45 years ago: The $4.03-an-hour rate recorded in January 1973 had the same purchasing power that $23.68 would today.

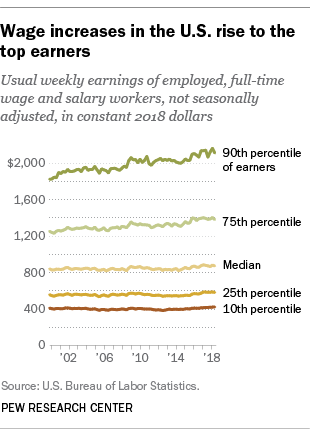

Here is Pew’s chart demonstrating the problem:

Because there’s been little growth in wages, the growth in the standard of living for those below the 90th percentile has been largely fueled by additional consumer debt. The WSJ reports that consumer debt, including credit cards, auto and student loans and personal loans, is on pace to top $4 trillion in 2019, the highest in history. Debt allows you to furnish your home, pay for education, and get a car without having to save for them. In that way, it supports the growing economy.

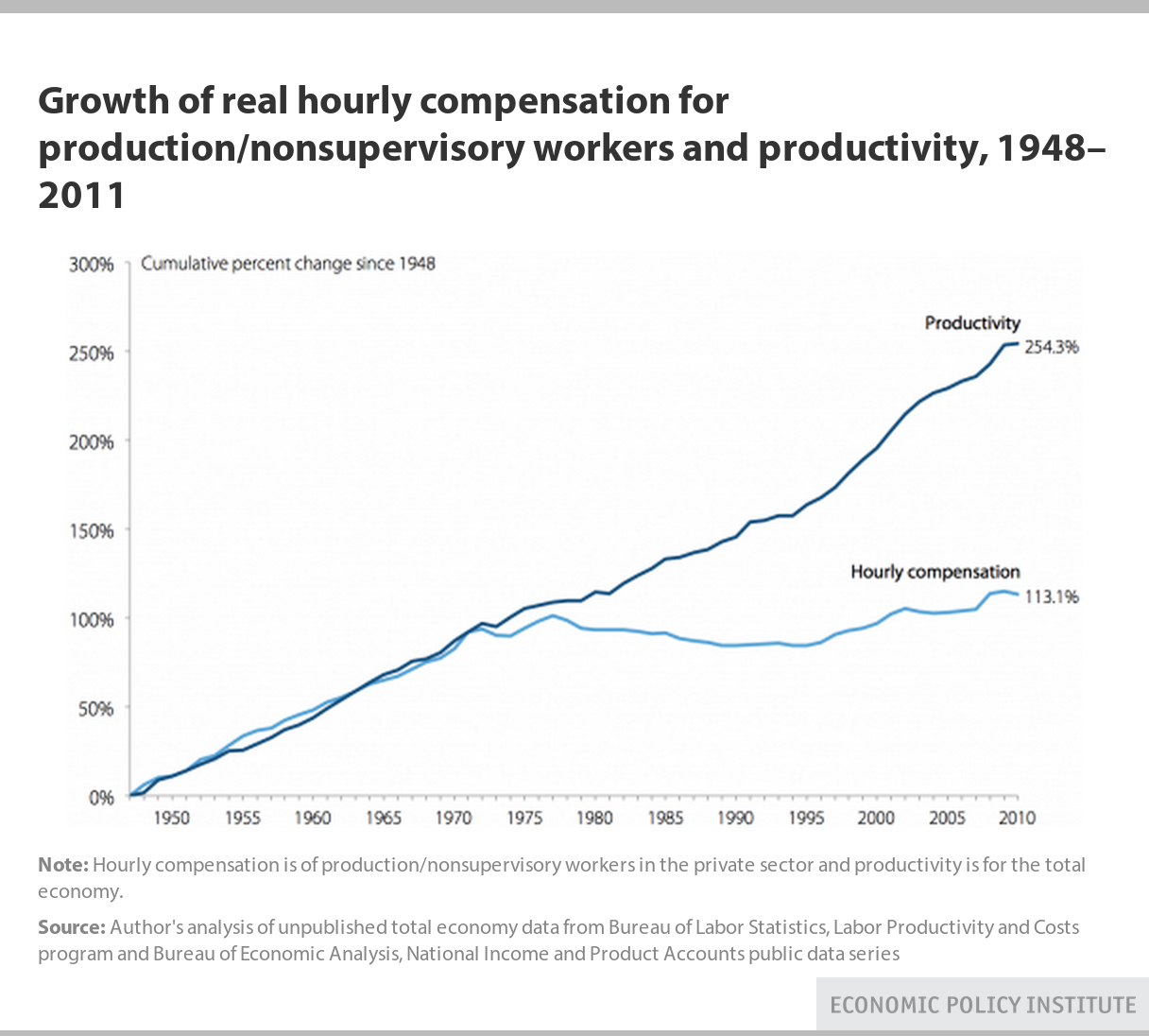

But Pew also shows how most of the income gains went to those at the top of the food chain:

Among people in the top 10th of the distribution, real wages have risen a cumulative 15.7%, to $2,112 a week – nearly five times the usual weekly earnings of the bottom tenth ($426).

This lack of symmetrical growth in debt and income actually matters. At some point household borrowers will default in greater numbers than they do today. When those losses occur, the monetary system won’t be able to bail out debtors (or banks) this time around as handily as we did in 2008.

Sluggish and uneven wage growth is a key factor behind widening income inequality in the US. Another Pew Research Center report found that in 2016, Americans in the top tenth of the income distribution earned 8.7 times as much as Americans in the bottom tenth ($109,578 versus $12,523).

Compare that to 1970, when the top 10th earned 6.9 times as much as the bottom 10th ($63,512 versus $9,212).

There is no simple solution to get American workers back on the right track. At a minimum, it will take a political groundswell aimed at overturning the way the tax code favors corporations. Along the way we will have to displace the political power of our corporate oligarchs.

Government must be made to serve the public interest, not Mr. Market.

Democracy is the sole mechanism enabling our citizens to have political and economic agency. But, democracy will cease to matter in a corporate-controlled, globalized system of government influence.