The Daily Escape:

Before tackling the major subject for today, Wrongo wants to briefly cover something you probably missed. There was an abortion ruling in Georgia that overturned the state’s anti-abortion law. The judge plowed new ground with his reasoning: (emphasis by Wrongo)

“While the State’s interest in protecting ‘unborn’ life is compelling, until that life can be sustained by the State — and not solely by the woman compelled by the Act to do the State’s work — the balance of rights favors the woman….Women are not some piece of collectively owned community property the disposition of which is decided by majority vote. Forcing a woman to carry an unwanted, not-yet-viable fetus to term violates her constitutional rights to liberty and privacy, even taking into consideration whatever bundle of rights the not-yet-viable fetus may have….It is not for a legislator, a judge, or a Commander from The Handmaid’s Tale to tell these women what to do with their bodies during this period when the fetus cannot survive outside the womb any more so than society could — or should — force them to serve as a human tissue bank or to give up a kidney for the benefit of another….When someone other than the pregnant woman is able to sustain the fetus, then — and only then — should those other voices have a say in the discussion about the decisions the pregnant woman makes concerning her body and what is growing within it.”

The ruling is unlikely to be the final word on abortion access in Georgia, since the case will ultimately be decided by the Georgia Supreme Court.

The judge has a solid argument: Why does society have an interest in a viable fetus when we know society won’t lift a finger to financially and medically support the newborn? Why allow the government to intervene at a time when the costs involved for the mother to continue with the pregnancy increase substantially?

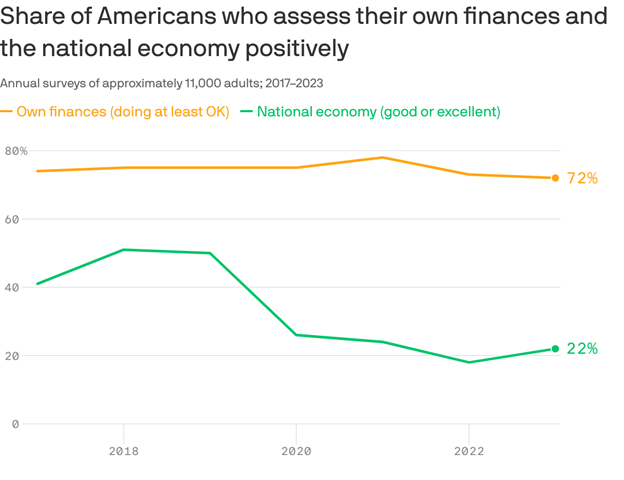

Let’s move to a powerful idea that emerged in the VP debate. Wrongo thinks the key to winning the election will be how Harris reaches out to Gen Z (those born between 1997 and 2012). PBS Newshour interviewed Kyla Scanlon, who reminds us that Gen Z now has more people in the workforce than the Boomer generation, but they aren’t faring as well. Scanlon says that Gen Z has had a tough go of it, being essentially born into the tech bubble, growing up during the Great Recession and then graduating or being in college during the pandemic.

From Scanlon: (brackets by Wrongo)

“…I think for a lot of Gen Z’ers, rent is definitely not as affordable as it used to be. Real wages have increased, so [have] wages adjusted for inflation, but rent has increased much more. And that’s sort of the foundation of how everyone experiences the economy. It’s where you live and how you have to pay for where you live….people look at the price of rent, they look at the price of gas, they look at the price of food, they just look at the inflation that we have experienced over the past few years, and it’s sometimes just not enough to even make those real wage gains worth it.”

More:

“It’s also the cost of childcare, eldercare, these things that are economically quite painful, but don’t necessarily show up in traditional economic measurements like GDP….They’re things that are… hidden costs that people experience.”

Scanlon also talked about the negative bias in the media that’s driving how people feel about their economic circumstances. Media sentiment on the economy has trended either skeptical or negative for a very long time, so people are reading negative headlines despite the economists and pundits saying the economy is OK. This is a big disconnect for the younger generations who get most of their news from social media.

In the debate, Vance said a few things that certainly resonate with Gen Z and others. He noted three things in particular:

- People are struggling to pay the bills. Times are tough.

- The American Dream is fading, and feels unattainable.

- We should stop shipping jobs offshore.

It’s hard to disagree with any of that, and Harris shouldn’t cede any of this ground to Trump. How hard is it to build this into your stump speech? She could easily acknowledge that we’re in the midst of a global cost of living crisis. The biggest one in half a century.

But it was left to Vance and Scanlon to say the things that most Americans feel.

Gen Z and their younger cohorts mistakenly think that the economy is a zero sum game, meaning that if China is doing well or immigrants are coming here and finding work, that regular Americans must be doing worse, even though the economic statistics say otherwise.

Harris needs to deliver an economic message that’s grounded in the reality that Gen Z and others are experiencing. It can be as simple as acknowledging what Vance or Scanlon called out as problems for many younger Americans.

All she needs to do is “Just Say It”.

Many of Wrongo’s 12 grandchildren (17-32 years-old) largely feel that the American Dream is beyond their reach. They’re certain Social Security won’t be there for them. Most think that they’ll never own a home.

Why can’t Harris speak to this? Harris and the Dems talk vaguely about “the opportunity economy” but a more emotional and empathetic call out is required. People with economic problems need to trust the head of the ticket, and that trust starts with acknowledging their reality: That things aren’t as good for the younger generations as the economic statistics say they are.

The Dems have an actual track record: Investing in infrastructure and encouraging domestic production of strategic goods. Investment in manufacturing is at an all time high. We’re starting to produce advanced chips in Arizona. Unions are stronger than in recent years.

Harris needs to show empathy for those in Gen Z (and younger) who are not fully participating in the opportunity economy.

It will help her win in November.