The Daily Escape:

Stoney Brook Grist Mill, Brewster, MA – February 2024 photo by Michael Kerouac

Wrongo and Ms. Right spent Sunday with one of our daughters and son-in-law. We spoke about the Ezra Klein op-ed in the NYT about why Biden should step aside. One of Klein’s points is that in presidential campaigns, the candidate is always the campaign’s biggest asset, and that Biden isn’t being used by Democrats as if he is their biggest asset.

Elsewhere, some pundits are saying that the Democrats need to forget campaigning on policy: Dems always try to find things people like and tell them they’re going to help them — and after that, show them the candidate’s character, biography, and qualifications for office.

Instead, the Republicans campaign by appealing more to emotion than intellect, using a negative message to develop enthusiasm.

While Wrongo is happy that Dems want to campaign again on an anti-Trump message, he still thinks policy is the right way to appeal to at least two types of voters: Those who rarely vote, and those who voted Democratic last time but are less enthusiastic this time. These voters think our political system hasn’t produced results for them, and they’re looking for promises to change that in order to get their votes.

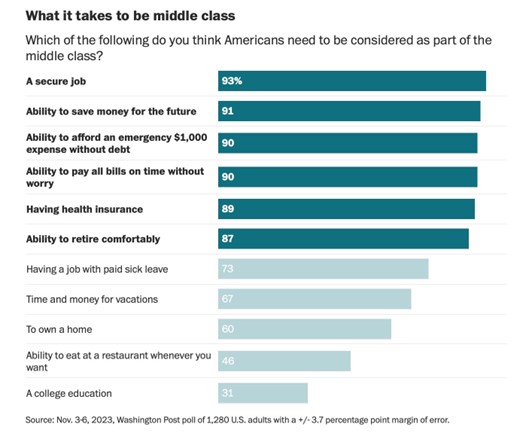

While we keep touting Biden’s economic performance, Wrongo recently found a very important poll taken last November by the WaPo that asked Americans how they defined being in the middle class:

“About 9 in 10 US adults said that six individual indicators of financial security and stability were necessary parts of being middle class….Smaller majorities thought other milestones, such as homeownership and a job with paid sick leave, were necessary.”

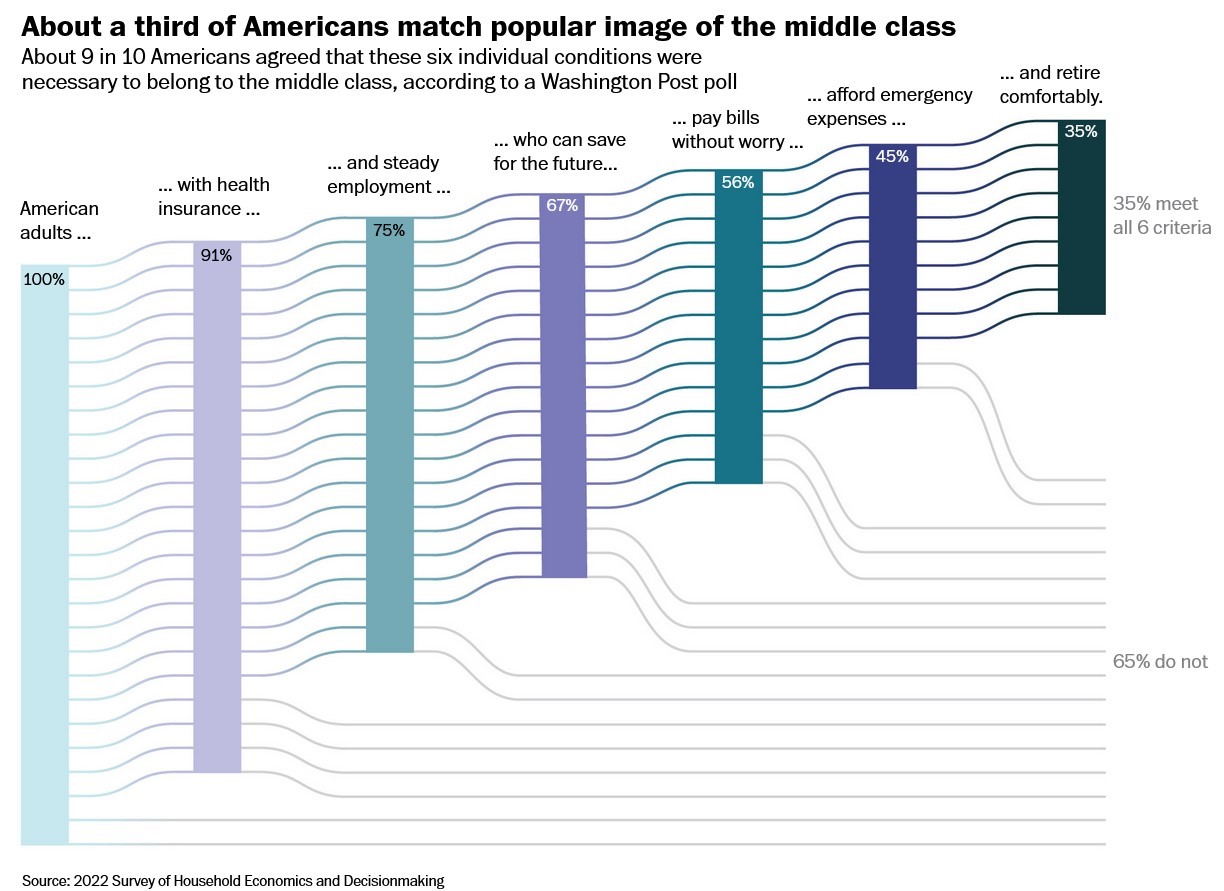

They also asked how many of those markers of being in the middle class people said they had achieved, and the results are a staggering rejection of how well the US economy is working for many people:

“Just over a third of Americans met all six markers of a middle-class lifestyle. While about 9 in 10 Americans had health insurance, only three-quarters had health insurance and a steady job. With each added measure of financial security, more Americans slipped away from the middle-class ideal.”

Let’s get into the findings. Here’s the WaPo chart about what factors Americans think it takes to be in the middle class:

It’s arbitrary to pick six, but they were the most frequently mentioned. A secure job. The ability to save. To afford an emergency. Paying the bills without worrying. Healthcare. Retirement. It’s a sensible list. And in the poll, huge majorities agreed those are the key criteria for a middle class life.

The Very Big Problem with this is that when the WaPo asked the same respondents if they had the ability to meet those criteria, the numbers are startling. Here’s the second WaPo chart:

Just 35% of people say that they meet the criteria that almost everyone, (~90%) agree should make someone middle class. If that’s true, America needs to redefine “middle” class. The majority in this survey did not have the financial security associated with being in the middle class. More from WaPo:

“The most common barrier was a comfortable retirement, something that about half of middle-income Americans over 35 felt they were on track to achieve.”

Think about what this research is really showing us. America no longer has a middle class. While ~90% of people agree on what a middle class life is, only a minority can afford it. This means we have a “phantom” middle class: Americans want to be middle class, but only a minority of them are. So what class does that make the majority?

What this research appears to show is that America is building something more like a permanent underclass.

Acknowledging this issue would be a great starting point for Biden to gain traction with low propensity voters and with the Gen X and younger voters who make up most of the low enthusiasm cohort of Democratic voters.

As Anat Shenker-Osorio puts it:

“Democrats rely on polling to take the temperature; Republicans use polling to change it.”

This time around the Democrats need to emulate Republicans who work at moving the needle instead of chasing it. And this middle class problem is an issue that will move the needle.

Fortune Magazine’s Tiffani Potesta writes that Gen Xers personify the problem of middle class life: (emphasis by Wrongo)

“Gen Xers expect to keep working longer than they planned–and will be the first generation to go into retirement with less financial security than their parents and grandparents.”

Gen X will be the first to reach retirement under a new paradigm: the widespread move from Defined Benefit plans to Defined Contribution or 401(k) plans in the US. This is a barely cited yet fundamental societal change that shifted the responsibility to save for retirement from employers to individual employees. More:

“…the numbers do not add up: Gen Xers reported that on average they will need roughly $1.1 million in savings to retire comfortably, yet they expect to stop working with only about $660,000 saved–a savings gap of around $450,000.”

Still more:

“According to a report from the National Institute on Retirement Security, the average account balance in 2020 for private retirement accounts among working Gen Xers was $129,994. This is woefully short of the amount of savings most of us will need to be secure in retirement.”

What’s worse is that the median account balance was scarier: $10,000–and 40% have zero savings.

For a society to be staring at the next few generations not being able to retire and not to be members of the middle class is very troubling, particularly in terms of what’s likely to happen if that’s the case. Losing our middle class is almost a sure path to autocracy, possibly through the rise of fascism and/or authoritarianism.

Biden and the Democrats need to acknowledge these problems are real and pledge to do everything possible to return America to having a true, bell-curve shaped middle class. They can run generally against Trump as “order vs. chaos”, but Trump is running on “America’s decline”, which includes the financial insecurity of millions of Americans. Biden needs to call that out specifically, along with ideas on how to fix the problem. That would make financial insecurity an issue for Democrats equal to abortion, something that targets a specific group and encourages them to get to the polls in November.

If Bernie Sanders isn’t too old to rage against economic insecurity, then Biden is old enough to do the same.