The Daily Escape:

Sunset at Fonts Point, Anza-Borrego Desert SP, CA – March 2024 photo by Paulette Donnellon

“If you want to live like a Republican, vote for a Democrat.” – Harry S. Truman

Republicans always claim that they are the Party of prosperity. They pretend that their policies lift everyday workers and their families, what with tax cuts and all, and the public seems to buy it. In polls, the Republicans usually get better marks on the economy than Democrats, often by hefty margins.

But as John E. Schwarz notes in the Washington Monthly:

“What is truly startling is the astonishing degree to which American workers have fared better under Democratic than Republican presidents….Today, the economic data are unambiguous: Whether it’s real wage gains or job creation, average Americans have fared far better under Democratic than Republican presidents.”

From the economist Jeffery Frankel, Professor of Capital Formation and Growth at Harvard University, and formerly a member of the White House Council of Economic Advisers:

“Since World War II, Democrats have seen job creation average 1.7 % per year when in office, versus 1.0 % under the GOP. US GDP has averaged a rate of growth of 4.23% during Democratic administrations, versus 2.36% under Republicans, a remarkable difference of 1.87 percentage points. This is postwar data, covering 19 presidential terms—from Truman through Biden. If one goes back further, to the Great Depression, to include Herbert Hoover and Franklin Roosevelt, the difference in growth rates is even larger.”

Frankel says that the results are similar whether one assigns responsibility for the first quarter of a president’s term to him or to his predecessor. He also makes the point that the average Democratic presidential term has been in recession for 1 of its 16 quarters, whereas the average for the Republican terms has been 5 quarters, a startlingly big difference.

Frankel asks whether these stark differences in outcomes are simply the result of random chance? But he concludes they aren’t:

“The last five recessions all started while a Republican was in the White House (Reagan, G.H.W. Bush, G.W. Bush twice, and Trump)….The odds of getting that outcome by chance, if the true probability of a recession starting during a Democrat’s presidency were equal to that during a Republican’s presidency, would be (1/2)(1/2)(1/2)(1/2)(1/2), i.e., one out of 32 = 3.1%. Very unlikely.”

I know, nobody said there’d be math in the column. Frankel says that the result is the same as the odds of getting “heads” on five out of five consecutive coin-flips. And it gets worse if we look back further in time:

“A remarkable 9 of the last 10 recessions have started when a Republican was president. The odds that this outcome would have occurred just by chance are even more remote: one out of 100. [That is, 10/210 = 0.0098.]”

More math, but you get the idea. If you look at job growth, the results are similar. More from John Schwarz:

“The significant contrast between each party’s record on wage and job growth has held true from the election of Ronald Reagan in 1980 through to the onset of the pandemic, just after 2019 ended, and after that, starting once again under Joe Biden.”

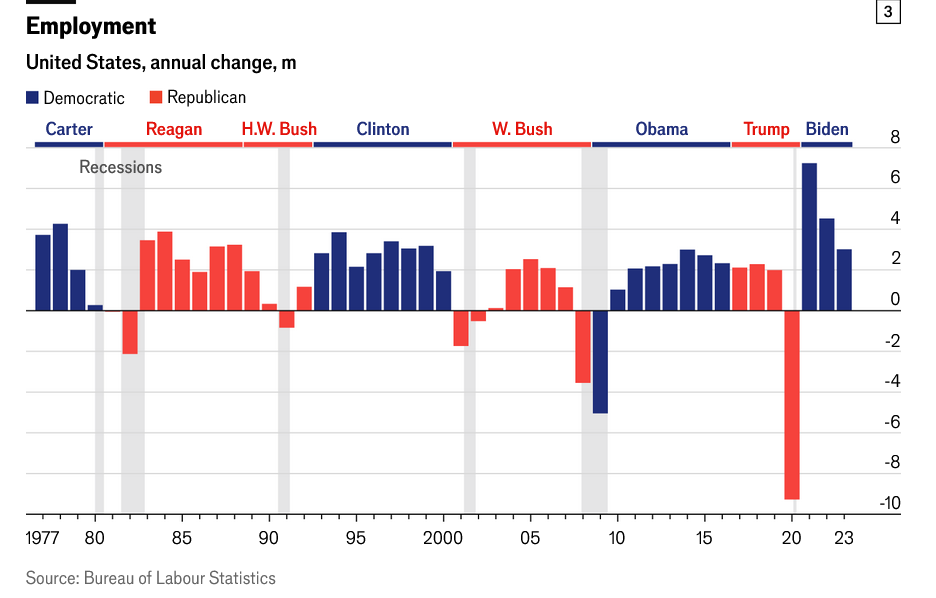

Here’s a chart from The Economist:

The Republican and Democratic Parties were in the White House for roughly equal amounts of time, 24 years each. During the Republican presidencies they created about 17 million jobs, whereas Democrats presided over the creation of about 60 million. That’s such a big gap that Americans can safely reject claims of stronger economic performance under Republicans.

Schwarz closes with this:

“Democrats have an amazing story to tell in 2024. They should tell it loud and clear.”

Absolutely!

Enough of the hard math. It’s time for our Saturday Soother, when we try to disconnect from Trump’s Bible sales and from the plan by Senate Republicans to introduce articles of impeachment of the Secretary of Homeland Security when there’s so much truly pressing business for them to consider.

Here on the Fields of Wrong, we’re attending to some spring yardwork in the precious time between passing rain and snow showers. We will also find the time this weekend to watch college basketball’s March Madness.

To help you focus on anything but politics on this Easter weekend, grab a seat by a south-facing window and listen to Gregorio Allegri’s “Miserere mei, Deus” (Have mercy on me, O God), performed here in 2018 by the Tenebrae Choir conducted by Nigel Short at St. Bartholomew the Great Church, in London.

Allegri composed this in the 1630s, during the papacy of Pope Urban VIII. The piece was written for use in the Tenebrae service on Holy Wednesday and Good Friday of Holy Week. Pope Urban loved the piece so much, that he forbid it to be performed elsewhere outside of the Sistine Chapel.

We all could use a little mercy now, and this is beautiful: